Pension fund payout: Pros and Cons (2026)

In certain life situations, it might make sense to consider withdrawing your pension fund. Although the pension fund, as part of the second pillar, is intended for your retirement provision in Switzerland, using the saved capital can be worthwhile — for example, for buying a home or starting your own business.

In this article, you’ll learn about the advantages and disadvantages of an early pension fund withdrawal. We’ll also look at whether, upon retirement, it makes more sense to receive your pension fund as a lump-sum payout or as a monthly pension. Let’s go!

Table of Contents

- Pension fund payout: Pros and cons

- Quick recap: What is the pension fund?

- In which cases do people consider withdrawing their pension fund?

- What are the pros and cons of early pension fund withdrawal?

- Should I draw my pension fund as a monthly pension or as a lump sum in retirement?

- Conclusion

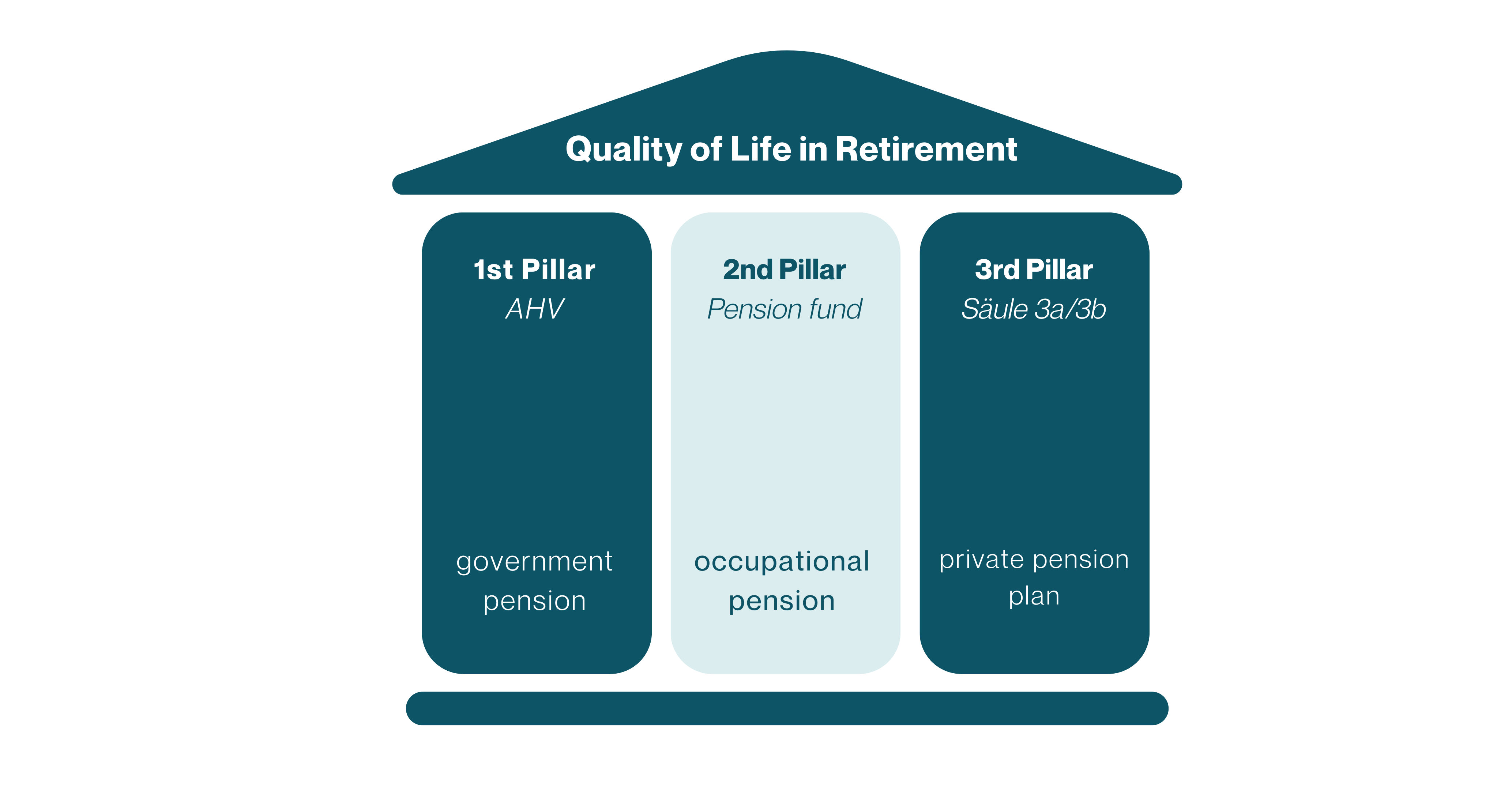

Quick recap: What is the pension fund?

The pension fund, also known as the second pillar of the Swiss pension system, is a key component of retirement planning. It complements the first pillar (AHV / IV) and is designed to ensure that you can maintain your usual standard of living in retirement.

The pension fund is an occupational pension system that is jointly financed by employers and employees. It is designed to provide an additional retirement income on top of the state pension from the first pillar. All employees who earn at least CHF 22'050.- per year are required to contribute to the pension fund.

In certain cases, it is possible to request an early withdrawal of the pension fund. We’ll look at those in the next section.

In what situations might you consider withdrawing your pension fund?

An early withdrawal of the pension fund is possible in four situations:

- If you want to buy a home

- If you plan to become self-employed

- If you are emigrating from Switzerland – though the full pension fund can only be paid out if you move outside the EU/EFTA countries; otherwise, only the non-mandatory portion can be withdrawn

- If you want to take early retirement (e.g., at age 58)

In all of these cases, there are strict rules and regulations that must be followed. You can find more detailed information on each scenario on the website of the Swiss Confederation.

What are the advantages and disadvantages of an early pension fund withdrawal?

I assume that one of the four scenarios applies to you right now, which is why you're exploring the topic of pension fund withdrawal. To help you make the right decision regarding your pension fund, here’s an overview of the advantages and disadvantages of withdrawing it early:

|

Advantages |

Disadvantages |

|

The accumulated capital can be used to start a business, reducing or eliminating the need for external funding. |

It creates a retirement savings gap, especially in old age, and sometimes also in the event of death or disability, which must be compensated for through insurance or investments. |

|

More equity is available for buying a home, which can lead to better financing conditions. |

A taxable event is triggered upon payout: as soon as the amount is withdrawn, capital withdrawal taxes or withholding taxes (if the payout occurs abroad) become due. |

|

After emigration, you no longer have a large amount of capital tied up in Switzerland and can either pay into a new pension system or use it for private retirement savings. |

Should I withdraw my pension fund as a lump sum or as monthly payments in retirement?

Another important question is whether you should withdraw your pension fund as a monthly annuity or as a one-time lump sum when you retire. This decision is highly personal and depends on your individual circumstances such as your partner, number of children, and total assets.

To help you decide, here’s an overview of the advantages and disadvantages of both options:

|

Advantages of lump-sum withdrawal |

Disadvantages of lump-sum withdrawal |

|

One-time taxation with a capital withdrawal tax (lower rate than regular income tax) |

Requires discipline and careful management to ensure the money lasts |

|

More flexibility, as the full amount is available – ideal if you have shorter life expectancy |

Uncertainty about the total amount needed for the rest of your life. This can be estimated with good pension planning, but requires regular updates. |

|

One spouse can opt for annuity, the other for lump sum |

|

|

Can be inherited freely |

|

|

Can potentially be invested more profitably to maintain purchasing power against inflation |

|

Advantages of annuity |

Disadvantages of annuity |

|

Lifetime guaranteed income – ideal if you expect to live long |

Ongoing taxation as regular income at your personal income tax rate |

|

Widow’s/widower’s pension of 60% of the deceased’s pension |

Fixed monthly payments leave little room for flexibility or large expenses |

|

Children in education receive 20% of the pension |

Cannot be inherited by adult children who have completed their education |

Conclusion on pension fund payouts

In summary:

Annuity withdrawal makes sense if the person:

- Has no heirs

- Has a high life expectancy

- Needs the pension to cover basic living expenses and has no other income sources

- Has little experience managing investments

Lump-sum withdrawal makes sense if the person:

- Has children or dependents and wishes to leave an inheritance

- Is not reliant on the pension due to other income sources

- Has a shorter life expectancy

- Wants flexibility and to manage the capital independently

A combination of both is also possible, where part of the amount is withdrawn as an annuity to cover basic needs, and the rest is taken as capital and invested. For couples, one partner can opt for an annuity, and the other for a lump sum.

In any case, I recommend scheduling a comprehensive pension planning session with a specialist between the ages of 55 and 60. Many Swiss residents have around 50% of their assets in the pension fund, and with good planning, they can reduce taxes and create a sustainable financial strategy for retirement while also investing wisely.