Unemployed in Switzerland? What you need to know

With an unemployment rate of just 2.4%, Switzerland performs exceptionally well in international comparisons. Hardly any other country has such a high employment rate.

However, job loss can still happen — whether due to restructuring, health reasons, or accidents. This guide explains exactly what steps to take if you become unemployed and how to make sure you stay financially secure during this period.

Table of Contents

- Unemployed in Switzerland? How to secure yourself properly now

- Unemployment as an opportunity: Starting your own business

- How well are you covered during unemployment?

- What happens if you get sick or injured while unemployed?

- Protection during unemployment (Mini Checklist)

- Conclusion

Unemployed in Switzerland? Here's how to protect yourself properly

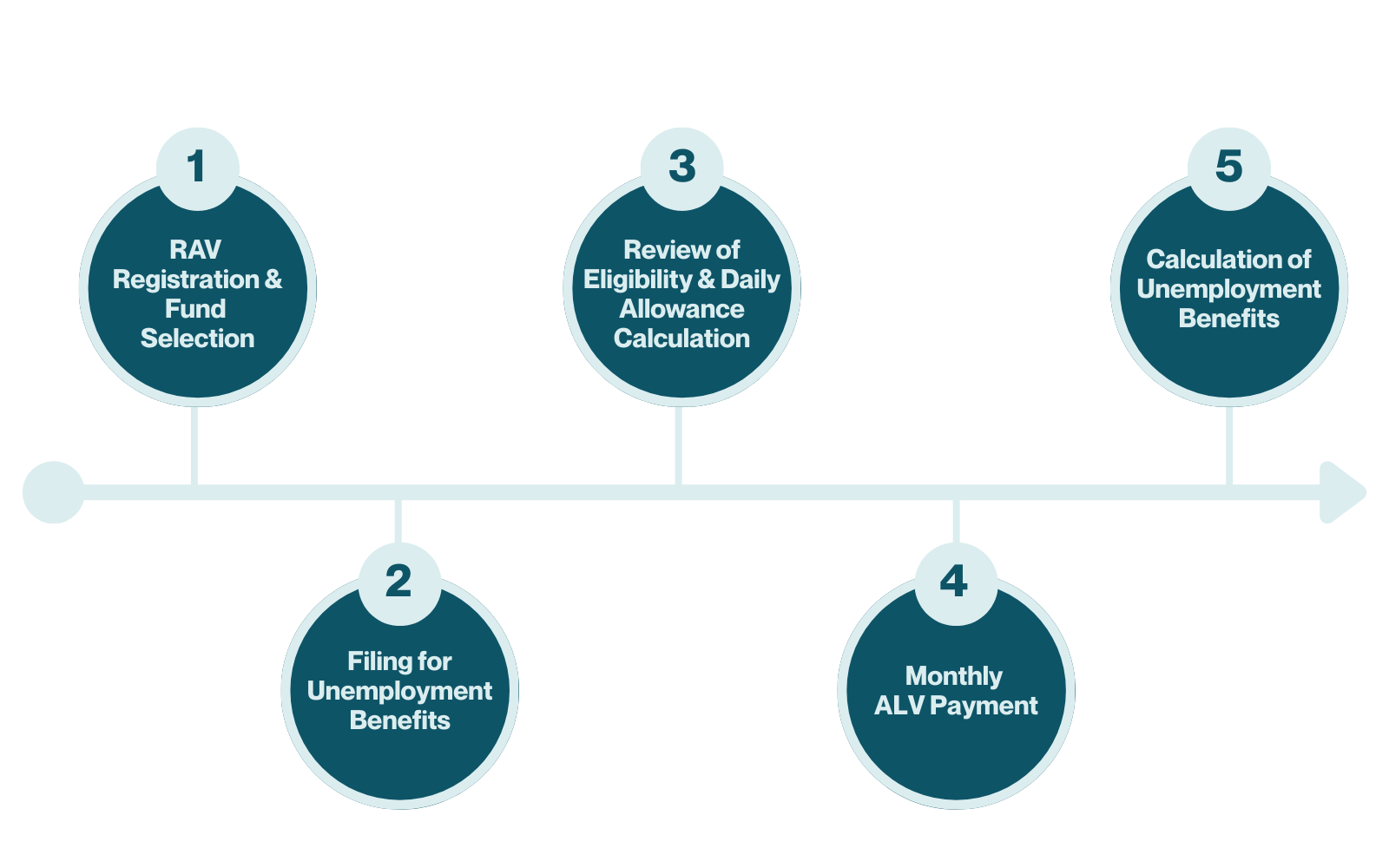

If you’re currently unemployed or about to lose your job, don’t freeze in shock. It’s important to take immediate action. The following graphic gives you an overview of the most important steps and their correct order:

Step 1: register with the RAV and choose your unemployment fund

Your first step? Register with the responsible RAV (Regional Employment Center). This registration ensures that you can start receiving unemployment benefits as soon as possible. The RAV also informs you about your obligations and helps you with your job search. You can register even during your notice period. This way you don’t lose any daily benefits, because unemployment compensation (ALV) only starts from the registration date.

⚠️ Important: Your entitlement to unemployment benefits only begins on the day you are no longer working for your old employer.

For registration with the RAV you will need the following documents:

- AHV card or health insurance card (or ideally a copy of the social insurance card)

- Swiss citizens: copy of the confirmation of receipt from the local municipality

- Foreigners: copy of your foreigner’s residence permit

- Copies of your employment contracts from the last several years

- Complete application dossier (resume, work certificates, diplomas, etc.), preferably also in electronic form

- Proof of job applications (if available)

Choosing an unemployment fund

When you register with the RAV, you will also need to choose an unemployment insurance fund (AL-Kasse). This fund will then be responsible for you: it calculates your unemployment benefit amount and pays it out to you monthly.

In Switzerland, there are both cantonal and private unemployment funds. In principle, their services are the same, but some may, for example, support further training more often or help you more intensively with job placement. Be sure to research and compare the different funds and their offerings carefully.

Step 2: applying for unemployment benefits

After you have completed your RAV registration and selected an unemployment fund, the RAV will check your entitlement to ALV benefits.

You are entitled to unemployment benefits if:

- You have been employed and contributed to unemployment insurance for at least 12 months in the last 2 years,

- Your main residence is in Switzerland,

- You have completed your compulsory schooling,

- You have not yet reached retirement age.

In addition, the RAV requires that you:

- Are immediately available for a suitable job (based on your qualifications and work experience),

- Begin job searching already during your notice period (for fixed-term contracts, 3 months before the end of the contract).

Step 3: Determine Your Entitlement and Calculate Your Daily Benefits

If the RAV approves your entitlement to ALV, the next step is to determine the amount and duration of your unemployment benefits.

How much unemployment benefit will you receive?

Your unemployment benefit is calculated based on daily allowances and your insured salary.

Usually, you receive 70% of your insured salary. Your insured salary is calculated based on your average salary over the last 6 months; or the last 12 months if that results in a higher figure.

Example

If you have an annual salary of CHF 100'000.-, then your average salary is:

CHF 100'000.- / 12 months = CHF 10'000.- per month

CHF 10'000.- x 6 months = CHF 60'000.-

You would receive 70% of your monthly CHF 10'000.- salary = CHF 7'000.-.

You receive 80% of your insured salary if:

- You have children under 25,

- Your insured salary is under CHF 3'797.-, or

- You have a disability degree of at least 40%.

The maximum insurable salary is CHF 148'200.- per year. This means that if you earn more than CHF 148'200.- annually, you will receive a maximum of 80% or 70% of CHF 148'200.-, which equals:

- CHF 118'560.- (80%)

- CHF 103'740.- (70%)

You will receive 5 daily allowances per week – from Monday to Friday. Since each month has a different number of weekdays, the total monthly payment may vary.

Looking again at the example above: We divide the CHF 7'000.- by the average number of working days (22) = CHF 318.- per day (Taggeld).

How long do you receive unemployment benefits?

Depending on your personal situation, you may be entitled to more or fewer daily allowances. The following table shows what applies to you:

|

Contribution Period |

Age / Maintenance Obligation |

Conditions |

Daily Allowances |

|

12 to 24 months |

Up to 25 without dependents |

- |

200 |

|

12 to <18 months |

From 25 |

- |

260 |

|

12 to <18 months |

With dependents |

- |

260 |

|

18 to 24 months |

From 25 |

- |

400 |

|

18 to 24 months |

With dependents |

- |

400 |

|

22 to 24 months |

From 55 |

- |

520 |

|

22 to 24 months |

From 25 |

Receiving a disability pension with a disability degree of at least 40% |

520 |

|

22 to 24 months |

With dependents |

Receiving a disability pension with a disability degree of at least 40% |

520 |

|

Exempt from contribution |

- |

- |

90 / 180 |

⚠️ Important: Waiting Periods Before You Receive Unemployment Benefits

You usually do not receive your unemployment benefit from day 1, but must expect certain waiting periods (up to 20 days). The number of waiting days depends on your insured income and whether you have maintenance‑obligated children:

Insured income without children:

- up to CHF 3'000.-: 0 waiting days

- CHF 3'001.- – 5,000.-: 5 waiting days

- CHF 5'001.- – 7'500.-: 10 waiting days

- CHF 7'501.- – 10'416.-: 15 waiting days

- CHF 10'417.- and above: 20 waiting days

Insured income with children:

- up to CHF 3'000.-: 0 waiting days

- CHF 3'001.- – 5'000.-: 0 waiting days

- CHF 5'001.- – 7'500.-: 5 waiting days

- CHF 7'501.- – 10'416.-: 5 waiting days

- CHF 10'417.- and above: 5 waiting days

Also keep in mind: if you resigned voluntarily, you may face 20–60 waiting days in which no ALV benefits are paid.

It is quite possible that the unemployment benefit will not cover all your monthly costs, since you only receive 70% (without children) or 80% (with children) of your last salary. Adjust your budget accordingly. Check whether you can renegotiate your health insurance, ongoing loans, and insurance premiums, etc. You could also conduct an insurance check to find better conditions.

The goal is not to give up everything, but to adjust your budget to your new situation — calmly and with a clear plan.

Step 4: Monthly ALV payments

Once your entitlement has been successfully reviewed and your daily allowances (Taggelder) have been calculated, you will soon receive your unemployment benefit (depending on waiting days and any sanction days). This will be paid out to you monthly by your chosen unemployment fund. Because not every month has the same number of working days, the amount may vary slightly from month to month.

⚠️ Important: You must attend all job applications and appointments with your RAV adviser to avoid sanctions (which lead to sanction days and no benefit payment).

Step 5: Final Settlement of unemployment benefits

If your daily allowances are exhausted (depending on your entitlement, between 9 and 29 months) and you still haven’t found a new job, you will be “de‑registered” from unemployment insurance. This means you no longer receive ALV benefits and must cover your living expenses from your own assets. If you are unable to do so or do not have sufficient assets, you will likely be entitled to other social benefits.

What does that mean in practice?

- If you do not have enough liquid funds (e.g., bank savings), you may eventually need to sell property.

- You may have to draw your AHV pension early, which is then permanently reduced by 13.6% (like a penalty).

- If available, you may have to liquidate pillar 3a accounts or vested benefits accounts. These amounts then count as assets and must be used for your living expenses.

Unemployment as a chance: starting your own business

You have the opportunity to become self‑employed during your unemployment and thereby end your unemployment status.

But beware: you must not have been self‑employed before. If you were previously self‑employed on the side and now want to start a different business full‑time, then this is allowed.

Once you inform the RAV that you want to become self‑employed, the so‑called “planning phase” begins. This lasts 90 days and allows you to develop your business idea without having to simultaneously apply for open positions. You can also attend training and courses that support your self‑employment. During the planning phase, you continue to receive your daily allowances.

After 90 days, you can decide whether to truly start your business. If not, you go back to “regular” unemployment and must apply for jobs, including those the RAV suggests.

⚠️ Important: This option is only available if you became unemployed through no fault of your own (e.g., you were laid off or the company went insolvent).

How well are you covered during unemployment?

Social insurance coverage in the 1st pillar

It’s very important to ensure your social insurance coverage during unemployment. That’s why your AHV, IV, and EO contributions continue to be covered automatically by the ALV as long as you receive daily allowances.

Occupational pension in the 2nd pillar

When you lose your job, you automatically leave your pension fund (BVG). You can then transfer your accumulated vested benefits (Freizügigkeitskonto) — your employer will ask you to do so. However, you must handle the set‑up of your vested benefits account yourself. Inform the pension fund about which account the money should be transferred to. A cash payout is only possible in exceptional cases (e.g., if you emigrate outside the EU/EFTA).

Tip: Compare vested benefits accounts — this can save you money. In our provider comparison, you can find the right account for you in just a few clicks.

⚠️ Important: If you have not transferred your vested benefits into a vested benefits account within 6 months after leaving the company, the money will be moved to a vested benefits institution. Your money is not lost, but you will need to track it. So take care of this early!

While unemployed, you continue to pay risk contributions for disability and death coverage, so you remain insured for these risks. However, you no longer contribute to the pension fund and therefore do not accumulate further retirement savings. You can voluntarily continue pension coverage with the vested benefits institution, but you pay these contributions yourself and they are not split 50/50 with an employer (as they would be during employment).

Private savings: pillar 3a

Even if your income is temporarily reduced, you should — if financially possible — continue to contribute to pillar 3a. Why? Because this actively prevents gaps in your retirement provision and also offers tax advantages.

You can only do this as long as you are receiving ALV benefits. After you’re deregistered from unemployment (no more ALV‑eligible income), you cannot continue pillar 3a contributions.

Unfortunately, it is not possible to withdraw your existing pillar 3a capital early just because you are unemployed. Early withdrawal is only allowed if you plan to buy or build property, leave Switzerland permanently, or become self‑employed.

|

Relevant Disability Degree (%) |

Percentage of Pension Entitlement |

|

0–39% |

0.0% |

|

40% |

25% |

|

41% |

27.5% |

|

42% |

30% |

|

43% |

32.5% |

|

44% |

35% |

|

45% |

37.5% |

|

46% |

40% |

|

47% |

42.5% |

|

48% |

45% |

|

49% |

47.5% |

|

50–69% |

The percentage matches the disability degree |

|

70–100% |

100% |

Example: Man born in 1969

-

Start of unemployment: 2022

-

Accumulated retirement savings (BVG) at the start of unemployment: CHF 250'000.-

-

Insured daily benefit: CHF 50'000.- (total for 12 months)

-

Age at start of unemployment: 53

Future credited retirement savings without interest:

(CHF 50,000 × 15%) × 2 = CHF 15'000.-

(CHF 50,000 × 18%) × 10 = CHF 90'000.-

Total: CHF 105'000.-

Relevant retirement savings for the calculation:

CHF 250'000.- + CHF 105'000.- = CHF 355'000.-

Multiply by the conversion rate of 6.8%:

CHF 355'000.- × 6.8% = CHF 24'140.-

→ this is the annual disability pension

You can close your income gap additionally (in the first year) with a daily sickness benefit insurance or alternatively a disability insurance. Disability insurance normally has a waiting period of 24 months before it pays benefits, but some insurers offer waiting periods as short as 3 months.

Accident: How you are insured

Your accident insurance coverage continues for up to 30 days after leaving your employer.

💡 Tip: After that, maintain your insurance cover by taking out a continuation accident insurance (Abredeversicherung) for up to 6 months. This also covers your daily benefits, which are usually higher than the ALV daily benefits because they are based on your previous salary, not the insured ALV salary.

This is important if you decide not to register with the RAV, for example because you plan to travel for a while.

Alternatively, you can include accident coverage in your health insurance. However, you still have to pay health insurance premiums. In that case, consider reducing your deductible (Franchise).

⚠️ Note: Health insurance only covers accident treatment costs — it does not pay daily benefits, as continuation insurance does.

What happens in case of death?

In the worst case — death — the AHV survivors’ insurance (1st pillar) applies. Surviving spouses can apply for a widow’s or widower’s pension. Orphan pensions for children are also provided.

The AHV pays 80% of the deceased person’s pension (widow/widower), or a 20% supplement to the surviving spouse’s own pension — whichever is higher. It also pays 40% of the deceased person’s retirement pension as an orphan pension until the child is 18 years old, or until 25 years old if still in education.

Depending on your situation and insurance status, additional benefits can come from the accident insurance (UVG) or your pension fund (BVG; 2nd pillar).

The UVG (accident insurance) pays — as the name suggests — only in the event of an accident. It provides 40% of the insured salary for the widow/widower and 15% for orphans. Combined with IV, UVG never pays more than 70% of the insured ALV salary.

In the case of illness, the picture is different: the pension fund (2nd pillar) typically pays 60% of the deceased person’s pension (widow/widower) and 20% for orphans.

Example: Man born in 1969 (continued)

Annual disability pension: CHF 24'140.-

- Widow’s pension (60%): CHF 14'484.-

- Orphan pension (20%): CHF 4'828.-

One‑time cash payout instead of pensions

In some cases widow’s and orphan’s pensions are not paid as monthly pensions but as one‑time capital settlements if:

- The disability pension is less than 10% of the minimum AHV pension (CHF 15'120.- per year),

- The widow’s/widower’s pension is less than 6% of the minimum AHV pension, and

- The orphan pension is less than 2% of the minimum AHV pension.

⚠️ Important: If these benefits are not sufficient for the surviving person, it can make sense to take out a term life insurance.

To find out how much you would receive from the different benefit pools, it’s worth carrying out a comprehensive pension and benefit analysis. This shows you, on the one hand, what you would receive in an emergency and, on the other hand, reveals gaps that you can cover with specific insurance.

💡 Good to know: In the Finelles Investment Class the 360° pension analysis (conducted by me) is an integral part of the program.

Protection during unemployment (mini‑checklist)

You clearly need to replan your finances during unemployment. But many forget to fully secure their personal insurance coverage while unemployed. To make sure you don’t forget anything regarding personal insurance cover, here’s a small checklist:

- Take out a continuation accident insurance for the next 6 months as a bridge. It covers both accident treatment costs and daily benefits, because your accident insurance ends 31 days after leaving your employer.

- Transfer your vested benefits from your pension fund to a vested benefits account.

- Take out voluntary retirement coverage with the vested benefits institution.

- Take out a daily sickness benefit insurance in case you get sick during unemployment and do not have enough assets to cover your costs.

- Alternatively, take out disability insurance if your benefits would not be enough in case of disability.

- If you are married or have children, check whether you need a term life insurance policy for the event of death (especially if your family depends financially on you and survivor benefits are not sufficient).

Conclusion: your protection in unemployment - with a plan instead of panic

First of all: Inhale & exhale. Losing your job in Switzerland is often annoying, but there are many good solutions and protections for the unemployed and jobseekers. Try to look at the situation as calmly as possible and use the tips in this article to put together a structured plan.