Inheriting in Switzerland: What you need to know (2026)

Inheritance is a sensitive topic - not just because it involves the death of a loved one, but also because it raises many legal and financial questions: Who gets what? Are there mandatory shares in Swiss inheritance law? Do I have to pay inheritance tax? And what should I actually do if I’m about to inherit something myself?

In this article, you’ll get a clear overview of how inheritance in Switzerland works. You’ll learn what steps heirs must take, what to watch out for (especially when real estate is involved) and how to thoughtfully integrate your inheritance into your financial planning. I’ll also show you what arrangements you can make during your lifetime to ensure your own estate plan leaves no questions unanswered.

Table of Contents

-

Inheriting in Switzerland – Who receives the Estate?

-

What is included in the Estate?

-

Important documents in the event of Inheritance

-

How high is the inheritance tax in Switzerland?

-

What can be arranged before the inheritance case?

-

Inheriting property

-

You’re about to inherit or just inherited? Here’s what to do (Step-by-Step Guide)

-

Conclusion: Inheritance in Switzerland

-

Frequently Asked Questions

Inheriting in Switzerland: Who receives the estate?

In Switzerland, the rules around inheritance are clearly defined. If you don’t want the default legal framework to apply, you need to specify your wishes in a will or inheritance contract. However, keep in mind that you don’t have complete freedom to distribute your assets as you wish.

Statutory Order of Heirs

If no marriage contract, inheritance contract, or will exists, the law determines the legal heirs and their order.

The legal foundation for this is the parentelic system:

Explanation:

This means that it is first checked whether there are individuals from the 1st parentela (children or grandchildren). If yes, then they or their direct descendants inherit.

If the deceased person has no heirs in the 1st parentela, then it goes to the 2nd parentela (parents, siblings, nieces, and nephews). The order of inheritance flows from top to bottom: If you have children, they inherit — if not, then grandchildren. Your siblings only inherit if your parents are no longer alive.

⚠️ Important: Couples living in a cohabiting partnership (Konkubinat) are not covered by the statutory inheritance laws. In these cases, it is advisable to establish a will or inheritance contract so that you can leave something to your partner.

Once it is clear who will actually inherit, the distribution of the estate depends on the family constellation as follows:

- 1/2 goes to the spouse/partner if there are also descendants (1st class of heirs)

- 3/4 goes to the spouse/partner if there are no descendants, but there are heirs of the 2nd class of heirs (e.g. parents, siblings)

- All goes to the spouse/partner if only heirs of the 3rd class of heirs or no legal heirs at all are present.

Below is a graphic that shows very clearly which rule applies depending on whether you have children and whether you are married:

If you are not married and not in a registered partnership (regardless of whether you have children), your inheritance goes 100% to your children or, if there are no children, to your parents and their descendants (e.g. your siblings).

If you are married and have children, your children and spouse split your estate half and half. Without children, your partner receives 75% of your estate and 25% goes to your relatives (e.g. parents, siblings).

What is included in the estate?

Married couples

Before the exact inheritance and any specific CHF amount can be defined, it must be established what is personal property and what is marital property — this is only relevant for married couples. It depends heavily on the chosen matrimonial property regime. If you don’t have a marriage contract, participation in acquired property applies automatically. This distinguishes between:

- Personal property: What each spouse already owned before the marriage, for example your investment accounts or car. Personal property also includes inheritances, gifts, and personal belongings.

- Marital property (acquired property): Everything earned during the marriage — for example dividends, rental income, and salary.

To separate these in case of death, an inventory must be created. If assets can no longer be clearly categorized as personal or marital property, they are usually treated as marital property.

💡 My tip: Create an inventory of all your assets before you get married.

Once personal property and marital property are defined, 50% of the marital property and 100% of personal property become part of the estate, provided that the marital property regime applies — which is the case for married couples without a marriage contract.

If you do have a marriage contract and have chosen a different regime (e.g. separation of property or community of property), then different rules apply to inheritance:

- With separation of property, everything is treated as personal property — meaning your spouse does not receive an equalization share from the marital property upon your death, but only their share of the estate.

- With community of property, all assets are treated as marital property (except personal belongings), and 50% of the marital property goes into the estate.

⚠️ Important: With a marriage contract and a so-called allocation of inheritance (Vorschlagszuweisung), you can assign 100% of your marital property to your surviving partner and only leave your personal property to the estate. This way you prefer your partner over other statutory heirs.

If you also don’t want your personal property to be inherited, you must draw up a inheritance contract and your legal heirs (usually your children) must sign a renunciation of inheritance. This is only possible if your children are over 18 years old.

Singles

If we look at the parentelic system again, we see that single people without children pass 100% of their assets to their 2nd parentel: their parents.

- If both parents are still alive, each parent inherits 50%.

- If the parents are no longer alive, the inheritance passes to siblings, and if they are not alive, to nieces and nephews.

Since singles are not married (and thus do not have marital property), their entire assets are included in the estate.

The complexity of patchwork families

In patchwork families, where children from previous marriages are involved, the inheritance situation becomes even more complex.

In these situations, it’s especially worthwhile to seek advice and support from a marital and inheritance law specialist or a notary and to draw up agreements that clearly regulate the situation.

💡 Tip: You can find a family law attorney or notary, for example, here:

Attorneys:

https://www.erbrechtsinfo.ch/anwaltssuche/

https://www.getyourlawyer.ch/anwalt/erbrecht/

https://frauenzentrale-zh.ch/rechtsberaterinnen/

Notaries:

https://snv-fsn.ch/notarin-notar-finden

How can a will influence heirs and the amount of the inheritance?

If you disagree with the statutory rules, you can draw up a will to personalise how your estate is distributed.

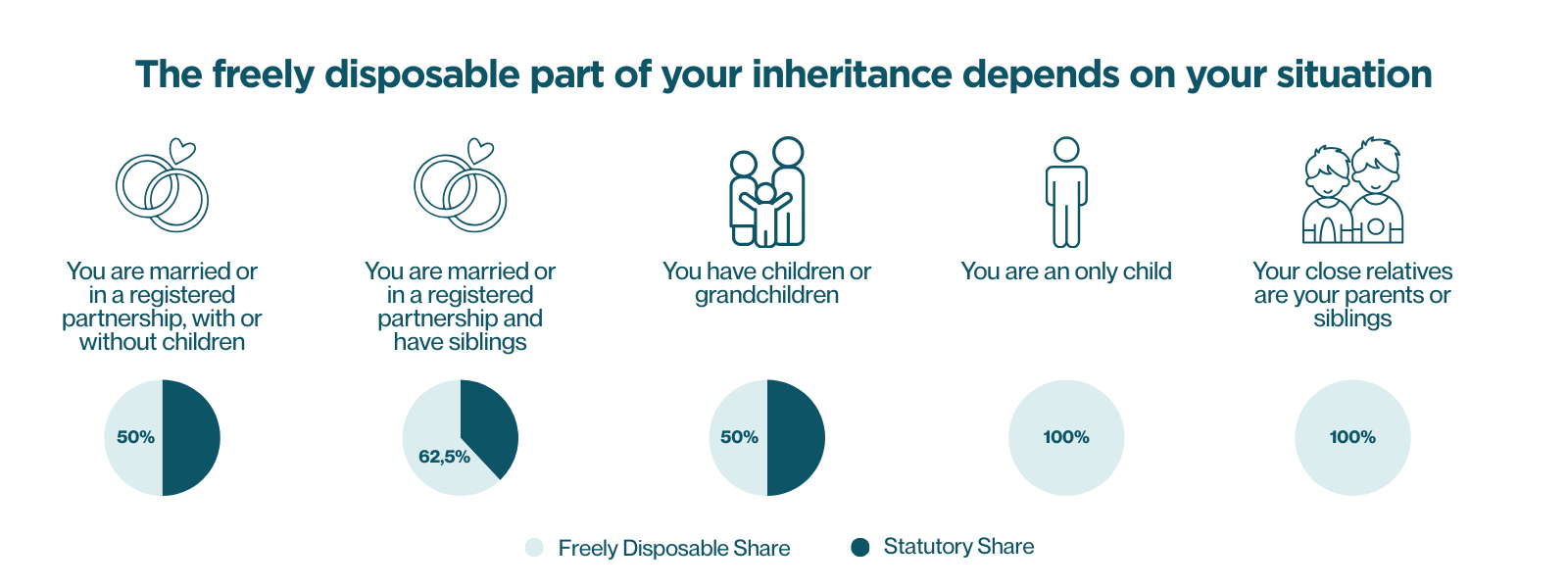

But be careful! You cannot freely bequeath your entire estate - statutory compulsory portions apply.

What does that mean?

Children and spouses are protected by compulsory shares and receive 50% of the statutory inheritance. You cannot change this even with a will.

All other heirs (e.g. siblings) are not protected by compulsory shares. These heirs can be completely excluded through a will. If heirs are assigned only their compulsory share or completely excluded, the remaining estate becomes the free portion.

When and how much of the free portion applies is shown in the following graphic:

What this means

You cannot completely exclude your spouse or life partner from your inheritance - they are entitled to 50% of the statutory inheritance.

You cannot completely exclude your children or their descendants from your inheritance either — they also receive a total of 50% of the statutory inheritance.

Example: You are married and have children, then you as the spouse would receive 50% of the estate and the children would receive 50%. If everyone is assigned only their compulsory portion, there would be a free portion of 50%, which the person who is bequeathing can distribute as they wish (e.g. to third parties).

You can use a will to benefit your cohabiting partner (within your freely disposable portion of the estate).

Parents or siblings can be excluded from the inheritance by will.

If you are unmarried and have no children, you can freely dispose of your entire estate — provided you have a will.

💡 Tip: To find out how large your personal freely disposable portion is, you can use the free will calculator from the Red Cross.

Important documents in the event of inheritance

Will

A will is a written document in which a person sets out, before their death, what should happen to their possessions and wealth after they die. It is a way to ensure that your own wishes are respected after death. It determines who inherits, what is inherited, and who administers the estate. A will must respect compulsory portions. It also follows strict rules: for example, it is only legally valid if it was handwritten or notarised.

Marriage contract

A marriage contract regulates the financial agreements between both partners. A marriage contract is voluntary. If both parties choose, they can sign it before marriage or afterwards.

It can define the property regime, adjust personal and marital property, such as categorising business shares as personal property, and also include an allocation of inheritance in favour of your partner.

The allocation of inheritance (Vorschlagszuweisung) is a contractual agreement that allows spouses to benefit each other in the event of death by awarding the surviving spouse the whole or part of the proposed share (half of the marital property). This means children and other heirs receive less in this case, and only receive more once the second spouse dies.

Inheritance contract

An inheritance contract is a binding contract you conclude with one or more people regarding your estate. All parties must agree, even if changes are to be made later or the contract is to be dissolved.

With an inheritance contract, you can also deviate from the normal statutory inheritance rules. For example, children can renounce their inheritance, but only if all persons entitled to a compulsory portion agree. That’s why an inheritance contract can only be concluded with people over 18 years old.

How high is inheritance tax in Switzerland?

Inheritance tax in Switzerland is very different depending on the canton:

- Obwalden and Schwyz don’t charge any tax at all.

- In other cantons and sometimes even at the municipal level taxes apply and vary based on the relationship.

Spouses, registered partners (same‑sex couples or “marriage for all”), and in most cantons also children/grandchildren are usually tax exempt, while more distant relatives like siblings can face 4-18% tax (e.g. in Zug, Zurich).

There are no uniform tax exemptions — each canton has its own thresholds. Direct descendants are often exempt in many cantons, but in some only partially.

Cohabiting partners must pay inheritance tax in most cantons. Some cantons have modernised their rules (e.g. Graubünden, Lucerne, Nidwalden, Uri, and Zug) and exempt cohabiting partners if they’ve lived together for at least 5 years. In Zurich, for example, there’s a tax exemption of CHF 50,000 if you’ve co‑habited for at least 5 years.

Want to go deeper? You can learn more about inheritance tax in Switzerland here.

⚠️ Important: Inheritance tax is due at the place of residence of the deceased (the person who bequeaths) — unless it’s real estate. For real estate, the tax is due at the location of the property, which can be advantageous, e.g., if the property is in Schwyz.

What can be arranged before the inheritance case?

One topic that arises during life before an actual inheritance event is the advance inheritance. For example, if children want to finance a home, parents can decide to pass on part of the inheritance before they die.

⚠️ Important to note: The equalisation obligation toward the other statutory heirs. At the later inheritance event, the value of the advance inheritance must be accounted for and compensated so that all heirs are treated fairly.

This can be especially problematic with real estate: Because the value for later distribution counts the market value at the time of your death, not the lower value at the time of the advance inheritance. If the property has appreciated, the child who received it must compensate the others for the higher value, which can be costly.

Inheriting a property

Real estate often makes up a large part of the estate and frequently causes discussions among heirs. To help you prepare, here are the key points:

Many parents gift the property during their lifetime to their children and retain a usufruct right — meaning they can continue to live in it.

However, for compulsory portion calculation, what counts is the value of the property at the time of death - not at the time of the gift.

Inheritance tax is charged at the location of the property (not the place of residence); properties in a canton like Schwyz may therefore be transferred tax‑free even if the heir lives elsewhere.

This can lead to financial imbalances: If one child receives the property and another receives liquid assets like a savings account, the property heir may have to make balancing payments to avoid violating compulsory portions.

You’re about to inherit or have just inherited? Here’s what to do (step‑by‑step)

If you’re in a situation where you are likely to inherit soon, there are several things to do. The checklist below shows you the most important points to watch out for.

⚠️ Important: The more that is arranged in advance, the easier the inheritance or estate settlement will go. Talk with your partner, children, and parents BEFORE it’s too late. This way you can discuss the most important issues without stress and plan what everyone wants in the event of death.

1. Review the estate

Start by getting an overview of the deceased person’s estate. For this, request a death certificate from the civil registry office and then from the responsible probate court or notary, an certificate of inheritance that identifies you as an heir. With this, you can prove your rights to banks, insurers, etc.

This is especially important if you are a direct heir: if your spouse or registered partner dies, your parents as an only child, or your siblings. If there are other statutory heirs (e.g. children from previous marriages), then you form an heirs’ community. As an heirs’ community, you all co‑own the entire estate of the deceased person.

As already described above, all personal property and 50% of marital property enter the estate (unless there is a marriage or inheritance contract). An inventory is needed to define both finally.

2. Appoint an executor

If the deceased person set up a will or inheritance contract, they might have appointed an executor. This person should be legally and neutrally qualified (e.g. a notary or lawyer) and is responsible for distributing and administering the estate.

If no executor was appointed, the heirs’ community is responsible for dividing and administering the inheritance.

3. Block accounts

If there’s no executor, contact the deceased person’s banks so that the accounts are blocked and protected from unauthorised access. Also consider any savings accounts and credit cards.

Important: Because the accounts are blocked, it’s wise for couples to have, in addition to a joint account for shared expenses, separate accounts — so the surviving partner can still access their own accounts and cover ongoing costs for a few months.

4. Decide whether to accept or renounce the inheritance

Check whether the inheritance is over‑indebted — meaning the deceased would leave you debts.

You have three months to renounce the inheritance. If you renounce it, your share goes to your statutory heirs, who can then also decide whether to accept or renounce. If all heirs renounce the estate, it is liquidated by the bankruptcy office.

If you do not act within three months, the inheritance is considered accepted. Then you are liable for the debts with the inherited assets.

5. Settle the estate

First, you must pay all outstanding bills of the deceased (e.g. rent, health insurance, taxes) from estate assets. If an executor has been appointed, that person will handle this.

Then notify all creditors (e.g. health insurance) of the death and terminate ongoing contracts such as rental, mobile, or insurance contracts. Many contracts terminate automatically upon death, but must still be actively notified.

Check if a will or inheritance contract exists. That determines how the inheritance is divided (see above: order of heirs and freely disposable estate). The inheritance is then distributed among the heirs — either by mutual agreement (inheritance division agreement) or, if there are disagreements, by an official partition.

For complex cases (e.g. involving property, foreign assets, or business shares), it’s worth getting help from a notary.

6. Complete formalities and notifications

Now it’s very important to claim the survivor benefits.

If the deceased person was your spouse or registered partner, check your entitlement to an AHV widow’s/widower’s pension. As a wife, this is currently paid for life (based on the deceased’s paid social security contributions). Why “currently”? The Federal Council is planning to reduce lifetime AHV widow’s pensions so that wives only receive payments until the children reach age 25.

As a husband, you are entitled as long as you support children under age 18. If you have a claim, register it with the AHV compensation office.

How high are the pensions?

- AHV: 80% of the deceased’s pension (widow/widower) or a 20% supplement to your own pension — whichever is higher. 40% of the deceased’s old‑age pension as an orphan’s pension until the child is 18 or until age 25 if still in education.

- Pension fund (2nd pillar): Usually 60% of the deceased’s pension (widow/widower) and 20% for orphans.

- Should the person die before retirement age, the values are based on the disability pension.

- Accident insurance (UVG): For accident cases, UVG pays 40% of the salary for the widow/widower and 15% for orphans.

⚠️ Important: A maximum of 70% of the deceased’s gross salary is paid out for AHV and UVG combined.

Also apply for an orphan’s pension if applicable

Apply for an orphan’s pension for children if it applies.

The civil registry office and the tax office should also be informed about the death. The tax office will also need information about how the assets are distributed.

What happens with children in the event of death?

If both parents have died or are deceased, the KESB (Child and Adult Protection Authority) becomes involved. Parents can use the right to propose a guardian during their lifetime, and the KESB will review the nominated guardian.

If this has not been specified, the KESB appoints the guardian.

The children manage the parents’ assets — under the supervision of the KESB — until they reach the age of majority.

At 18, they officially receive their inheritance.

7. Submit the inheritance tax return

As explained above, spouses and registered partners are usually exempt from inheritance tax. All other heirs (siblings, cohabiting partners in some cantons — except in Schwyz, distant relatives) must pay inheritance tax.

Check with your canton whether, and how much, inheritance tax applies and then submit the inheritance tax return so you can pay what’s due. You can calculate how much tax you owe here.

⚠️ Also important: A tax return for the deceased must be filed for the time from the beginning of the year until the date of death.

If the person was married, this is the last joint tax return of the couple — after that, the surviving partner must file a single tax return.

8. Adjust your own financial plan

It makes sense to incorporate the inherited assets into your existing financial planning. Especially if large sums are involved, this can significantly affect how you handle your money and build up your retirement provision.

But: only do this after you have legally inherited. Planning with the money prematurely is risky because a will, marriage contract, or inheritance contract can still change before the person dies.

Please also do not neglect your own retirement planning because you are sure you will inherit! A husband is not a pension — and an inheritance isn’t either.

You don’t yet have financial planning? Learn more about how I can support you as a certified financial planner here.

Decide whether you want to keep inherited property (for personal use or renting) or sell it. Take mortgages, maintenance costs, and property taxes into account in your calculations.

Check if inherited securities like stocks or ETFs fit your own investment strategy. Then weigh whether it makes sense to merge the portfolio with your existing one or sell and reinvest according to your strategy and risk profile.

⚠️ Caution: Depending on the bank or broker, high trading costs can apply. Check our online broker comparison to find the right provider for you and your inheritance.

If terms like investment strategy, ETFs, risk profile, sound like alphabet soup to you, then I recommend the Finelles Investment Class. There you learn these financial basics, create your own investment strategy with me, and also build your personal financial plan. We can directly include your inheritance and set a strategy for it. Learn more here and join the next round!

9. Use the inheritance wisely

Instead of immediately booking a 5‑star all‑inclusive family holiday, I strongly encourage you to use the inheritance in a way that benefits you and your finances in the long term. You’ve received a wonderful gift and should — also in the spirit of the deceased — make the most of it.

This can understandably cause stress, because you now find yourself in a situation where you have to make (often quick) financial decisions and you may be wondering how to handle them responsibly.

In my view, it makes sense to pay off any debts first (e.g. mortgage, loans) and build up your savings buffer (e.g. emergency fund or tax reserves).

Then use the difference to top up your retirement planning — by fully utilising pillar 3a, or, if you’re over 50, buying into the pension fund.

You can then invest the rest. If you have no experience with investing yet, download our Financial Boost eBook for free and discover why investing isn’t dangerous or something to be afraid of.

10. Update your own estate planning

Unfortunately, the death of someone close is always a reminder of our own mortality. Take this moment to create or revise your own will. Maybe your financial situation or life circumstances have changed and are no longer reflected in your current will. How to write a legally valid will is explained [here].

Also, have a conversation with your direct heirs or other people you might inherit from. Do you need an inheritance contract for that? It's especially useful when the inheritance situation is complex or there are emotionally difficult dynamics.

Conclusion: Inheriting in Switzerland

Whether you’re about to inherit or want to arrange your own estate: inheriting in Switzerland is more than just a formality. It’s about clear decisions, financial foresight, and often about emotional fairness.

Inheritance law in Switzerland is well-structured, but without a will or inheritance contract, things can get complicated — especially in modern family structures.

My tip: Start early with your own inheritance planning, and be prepared for the next steps if you become an heir. A clearly arranged estate, an updated financial plan, and a good understanding of your rights and responsibilities make all the difference — for you, your family, and your wealth.

Frequently Asked Questions about Inheritance in Switzerland

What amount is tax-free when inheriting in Switzerland?

That depends on your canton, because inheritance tax is regulated at the cantonal level, not nationwide. Spouses and registered partners are always tax-exempt, and in many cantons so are direct relatives such as children and grandchildren. Other cantons only grant tax-free allowances — a certain amount is tax-free, and the rest is taxed. It's best to check with your local cantonal tax office.

What is the legal share (Pflichtteil) for children in Switzerland?

The legal share for children is 50% of their legal inheritance. That means: if you have children, you can freely dispose of half of your estate, but the other half must go to your children — no matter what your will says.

Do children always have a right to their legal share?

Yes, generally speaking. The legal share can only be denied in very limited exceptions — for example, in cases of serious crimes against the deceased (e.g. attempting to kill the person leaving the inheritance). In practice, this is rare and requires a clear justification in the will. So if you want to prevent a child from inheriting, you need a legally valid exclusion of their legal share, otherwise the claim remains valid.

This also applies to children or relatives who live far away or with whom you no longer have contact.

How much can be inherited tax-free?

This also varies by canton. In cantons like Schwyz or Obwalden, there is no inheritance tax at all, so the entire estate is tax-free — regardless of its value. In other cantons, the tax-free amount depends on the degree of kinship and the size of the inheritance.

A general rule of thumb: the closer you are related to the deceased, the larger the tax-free portion, up to complete exemption.