Life insurance in Switzerland (2026): what you need to know

Life insurance isn’t the simplest topic—especially in Switzerland. I often get asked: Do I really need life insurance? And if so, which one is right for me—a pure term life insurance or a mixed policy?

In this article, I’ll walk you through everything you need to know about life insurance in Switzerland (2026):

- What types of policies exist and how they differ

- When life insurance is truly necessary

- Common mistakes and pitfalls—and how to avoid them

- Practical tips on how to find the right policy for you

By the end, you’ll be able to confidently decide if and which life insurance fits your situation—without paying for anything you don’t need. Let’s go!

Table of Contents

- What exactly is life insurance?

- Overview of the different types of life insurance

- When is life insurance necessary?

- Taxes & retirement: Life insurance in pillar 3a and 3b

- Conclusion on life insurance

- FAQs about life insurance in Switzerland

What exactly is life insurance?

At its core, insurance is always about covering a risk. In the case of life insurance, the risk in question is either your death or your inability to work.

If you die, you personally won’t benefit from the insurance—but your beneficiaries will receive a payout.

If you become unable to work, whether permanently or temporarily due to illness (like burnout) or accident, a disability insurance policy will pay you a monthly amount to replace lost income. Strictly speaking, this type of disability insurance isn’t considered life insurance, but it’s often sold as a combined package.

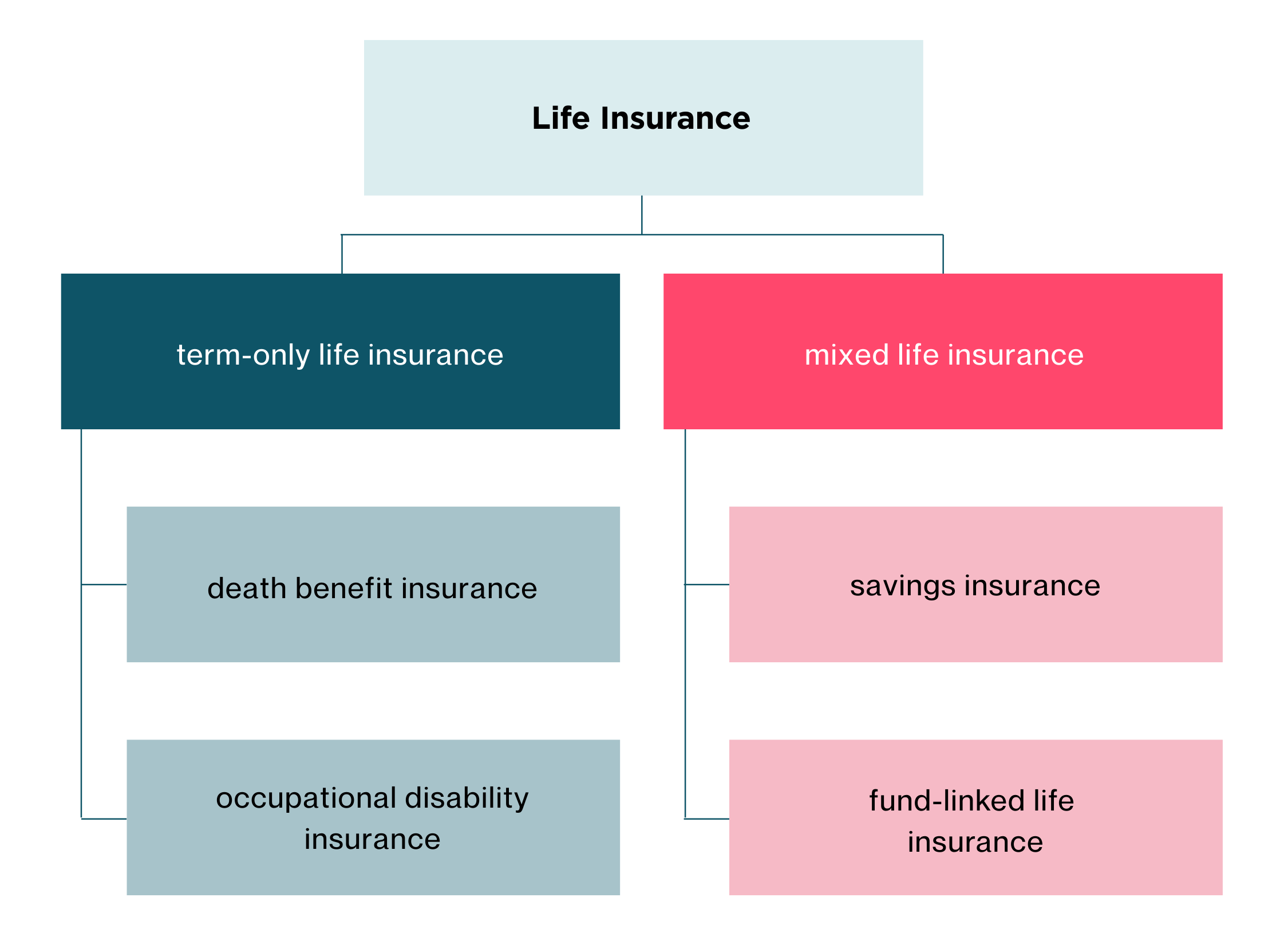

With life insurance, we distinguish between a pure term life insurance policy and a mixed life insurance policy.

Term life insurance is an individual policy that pays out a contractually agreed sum to your loved ones in the event of your death.

This makes sense if you have children or a partner who relies on your income (e.g. to pay off a mortgage).

Important: If you’re in a partnership or cohabiting relationship, a pure term life insurance policy is strongly recommended as protection—since the state provides fewer entitlements to each other in the event of death (e.g. no survivor’s pension from AHV, and often no payout from the pension fund or accident insurance either).

A mixed life insurance policy works in a similar way, but includes a savings component. If you reach the end of the policy term without needing the death benefit, you receive your accumulated capital instead. Why I don’t recommend this model—we’ll get to that in a moment.

Whether you need life insurance or not can only truly be answered with a comprehensive retirement and risk analysis. But I’ll explain in a moment when you definitely should have one.

Overview of the different types of life insurance

Pure term life insurance

Death benefit insurance

This insurance covers solely the risk of death. It’s especially useful when family members, business partners, or mortgages need to be financially protected. In other words, it only becomes relevant if someone is financially dependent on you—if you have children, co-own property, or are an entrepreneur.

Disability insurance

This policy pays a monthly pension if you become unable to work, either temporarily or permanently, due to illness or accident. It makes sense if the disability benefits from pillar 1 and pillar 2 are too low to cover your expenses. It’s not a classic life insurance policy but is often offered as an add-on module.

Mixed life insurance

Savings insurance

A mixed life insurance policy combines two or more components:

- Death benefit insurance: payout to your beneficiaries if you die during the term of the policy, and/or

- Disability insurance: annual pension payout in case of invalidity, plus

- Savings insurance (endowment insurance): payout of the saved capital if you reach the end of the policy term.

Important: I don’t recommend mixed life insurance. Insurance should be used to cover risks, not to save money or build wealth. That’s what pillar 3a and your investment portfolio are for.

Unit-linked life insurance (Anteilgebundene Lebensversicherung / fondsgebundene Lebensversicherung)

In this case, the savings portion of your premiums is invested in investment funds. The payout depends on the market value of those funds.

In principle, you can add a premium waiver to any of these combinations—meaning premiums will continue to be paid in case of disability. This is particularly sensible with mixed life insurance policies and disability pensions.

The following table gives you an overview of the pros and cons of the different models:

|

Product |

Advantages |

Disadvantages |

|

Disability insurance |

Flexible: You can cancel it once the risk no longer exists (e.g. once your income from pillars 1 and 2 is enough to cover your expenses). Cost: Pure disability insurance is significantly cheaper than a mixed life insurance policy. |

Limited benefit: Only the risk benefit is covered. If you don’t become disabled, the money is gone—just like with car insurance. |

|

Pure term life insurance |

Flexible: You can cancel it once the risk is no longer present (e.g. children have moved out, second mortgage is paid off). Cost: Much cheaper than mixed life insurance. Beneficiaries: You can freely choose your beneficiary, which is especially helpful in unmarried partnerships where you want to protect your partner. |

Limited benefit: The payout only occurs if the insured risk happens. Taxes: Payouts are subject to capital benefits tax, regardless of whether you are married or in a domestic partnership, and regardless of whether it’s a 3a or 3b policy. |

|

Mixed life insurance (savings + risk coverage) |

Premium waiver: Covers both the savings and risk portion. In case of disability, the insurer continues to pay into your policy. Alternatively, you could define your disability insurance high enough to cover your savings rate. Taxes (married): In a marriage, inheritance tax is usually not applied, so mixed life insurance can be advantageous compared to term life insurance. Applies only to pillar 3b, as pillar 3a is always taxed with capital benefits tax. |

Costs: Often charged upfront. If you cancel early, you incur high losses. Taxes (domestic partnership): Inheritance taxes apply to the surrender value/capital. Applies only to pillar 3b—pillar 3a is taxed through capital benefits tax. |

When is life insurance necessary?

In my opinion, there are three situations where life insurance is essential:

- If you have children who are not yet of legal age

- If you have purchased a property and still have an outstanding mortgage

- If your partner or someone else (e.g. your parents) is heavily financially dependent on your income

So, if you’re a single woman without children, you don’t need to worry about this for now. What’s probably more relevant in your case is the topic of disability insurance.

Unfortunately, an old myth still persists, and that’s why I want to say it clearly again: life insurance is not a product for retirement planning - let alone for long-term wealth building!

It’s one part of your personal risk coverage, to protect you in a worst-case scenario. But it’s not a building block that will help you live a comfortable life in retirement.

What applies to the self-employed?

For self-employed individuals, the same applies as for employees. If you have children and/or a mortgage, it makes sense to take out a pure term life insurance policy, so that your loved ones are not left in a difficult financial situation.

To protect yourself against potential insurance gaps in the event of lost income due to accident or illness, you can voluntarily contribute to a pension fund or alternatively take out a disability insurance policy within pillar 3a or 3b. Which is better depends on your income, industry and needs. This can be clarified in the course of a pension analysis and personalised financial planning.

Taxes & pension planning: Life insurance in pillar 3a and 3b

Depending on your life situation, it might make sense to take out life insurance under pillar 3a or pillar 3b:

Marriage: Inheritance tax is levied on the surrender value / capital. In a marriage, you generally don’t pay inheritance tax. That’s why mixed life insurance is often more advantageous compared to pure term insurance – because capital benefits tax applies instead. But this only applies to pillar 3b! Payouts from pillar 3a are always subject to capital benefits tax. At the same time, you can also invest your capital in a portfolio, and pass it on without inheritance tax to your spouse. That’s why it still makes sense to take out a pure term policy under pillar 3a, and pass on the remaining capital through your 3a or free private assets.

Domestic partnership: In pillar 3a, capital benefits tax is charged at payout – regardless of whether it’s a mixed or term policy. In pillar 3b, this applies if it’s a pure term life policy. With a mixed policy, inheritance tax is charged on the surrender value, which is usually higher than capital benefits tax. That’s why for couples in a domestic partnership, a pure term life policy under pillar 3a is generally the better option. You can also pass on other pillar 3a assets or private savings, though they may also be subject to inheritance tax.

General rule: If you take out a policy (e.g. disability or pure term life insurance), it’s usually advisable to do it under pillar 3a.

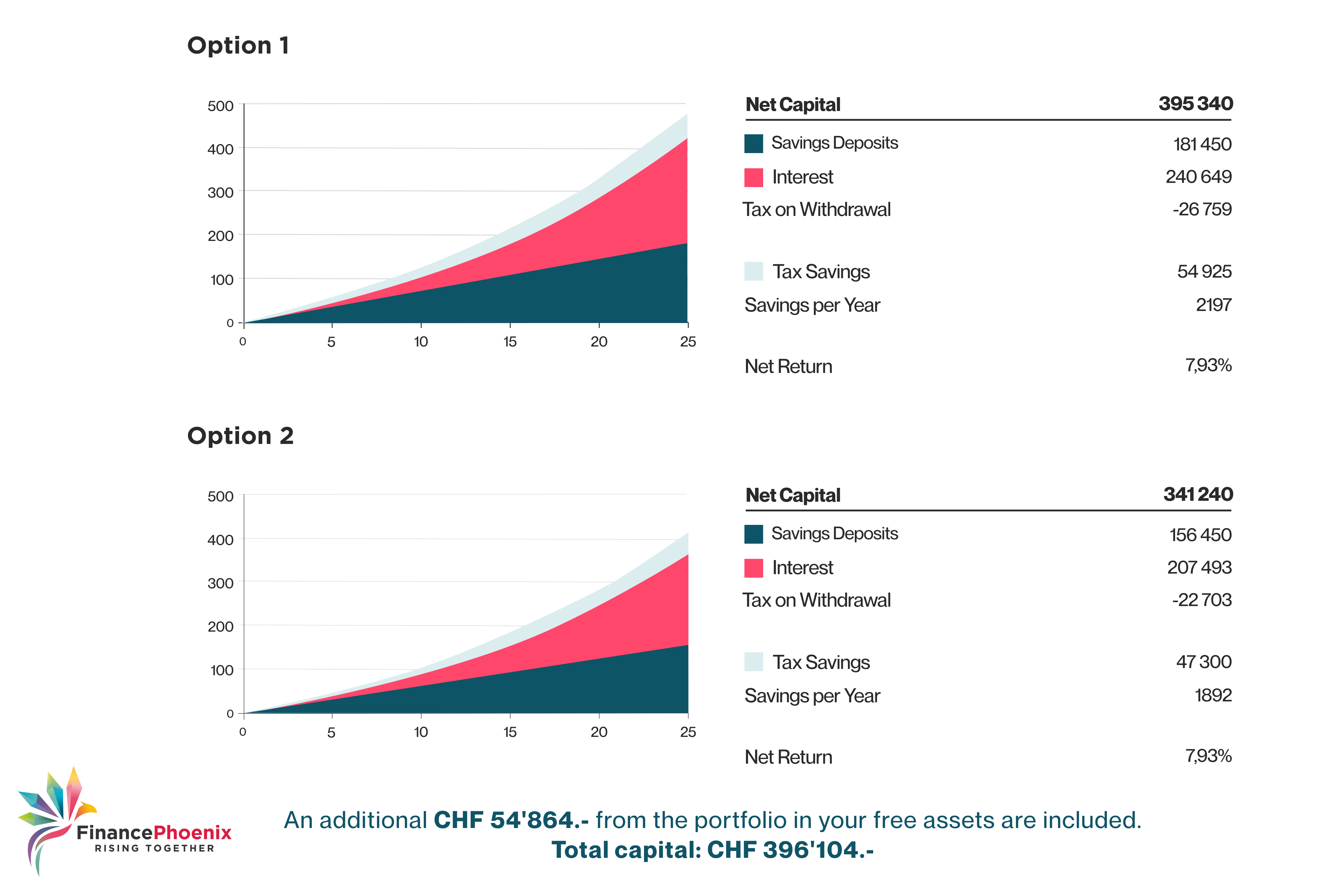

Let’s look at the value development over time:

Option 1: 3a and 3b

The maximum 3a contribution is fully invested in a 3a portfolio (e.g. finpension, VIAC), and the disability insurance is taken out under pillar 3b (costs e.g. CHF 1'000.- per year).

Option 2: Only 3a

The disability insurance premium (e.g. CHF 1'000.-/year) reduces the maximum 3a contribution of CHF 7'258.- to CHF 6'258.-/year – which is fully invested in the 3a portfolio(s). An additional CHF 1'000.- is invested in a private portfolio (outside of pillar 3a).

In both cases, you’re spending CHF 8'258.- per year: CHF 7'258.- in 3a and CHF 1'000.- in private assets. So, the tax deduction while contributing is the same.

The only difference: With option 2, you also pay wealth tax on your portfolio value and income tax on interest and dividends.

The invested capital remains the same, as you are still investing CHF 7'258.- per year overall.

At the point of payout, however, things look different.

In option 1, the entire 3a capital is taxed.

In option 2, only the amount saved in 3a (CHF 6'258.-/year) is taxed – so the total taxable 3a capital is lower, which reduces your capital benefits tax.

An additional CHF 54'864.- comes from the portfolio in free assets.

Total capital: CHF 396'104.-

You see then, from a purely tax perspective, it makes more sense to take out your life insurance within your pillar 3a.

Conclusion on life insurance

Life insurance isn’t a product for every woman, but in certain situations, it’s absolutely essential. If you have children, are paying off a mortgage, or your partner or someone else (like your parents) depends heavily on your income, a pure term life insurance can be crucial. In most cases, I recommend taking it out as part of your pillar 3a.

I personally advise against mixed life insurance: it’s expensive, intransparent, and not suitable for long-term wealth building. For your retirement planning, a pillar 3a investment account and investments in your free assets are much better choices.

What’s important (as always): don’t fall for slick marketing. Instead, evaluate your individual situation. Compare providers, check contract terms, insurance amounts and costs - and only insure what’s truly necessary.

That’s how you make sure your loved ones are protected in the worst-case scenario without wasting money on overpriced products.

FAQs on life insurance in Switzerland

How do I determine the right insurance amount for my life insurance?

The amount depends on which financial obligations you want to cover.

Example: In a couple with children, take your current budget and check how much will be covered through pillar 1 and 2 survivor benefits, and how much income the surviving partner will receive. The gap is what you want to cover. A common approach is to insure 70% of your current income. If one partner isn’t working, plan with around CHF 4'000.- per month for additional childcare or household help. Multiply the yearly gap by the number of years until the children are of legal age, and that gives you your coverage amount.

For disability insurance, the goal is to replace 90% of your current income from pillars 1 and 2. For accidents, this is usually already covered. But in the case of illness, you often need an extra private policy.

Tip: Don’t calculate too tightly - better to over-insure slightly and adjust downward later as the risk decreases.

Should I take out my policy in pillar 3a or 3b?

That depends on your life model:

- 3a: More tax-efficient, since you can deduct premiums from your income.

- 3b: More flexible and often better for married couples, because no inheritance tax is due in the event of death. But this only applies to mixed life insurance, which is usually not cost-effective compared to investing via an account. I rarely recommend 3b.

Important: Always compare both options in your personal situation (ideally with an expert like me) and consider taxes, beneficiaries, and flexibility.

How do I know what kind of life insurance I have?

- Death benefit: If your contract specifies a fixed amount to be paid out in case of death, it’s usually a pure term life insurance. You set the amount when the contract was signed.

- Disability coverage: Look for wording like "monthly benefit in case of disability due to illness and/or accident".

- Premium waiver: If the policy says "premium waiver in case of disability", it means you won’t have to continue paying premiums if you become disabled. If this isn’t in the policy, then the waiver is not included.

- Mixed insurance: If the contract includes phrases like "benefit in case of survival", "capital at retirement" or "benefit depending on savings", it’s a mixed life insurance. It may or may not be bundled with other elements like premium waiver or disability insurance.

Also, you can often identify the components by how the premium is split, as insurers typically break down each part.

What happens if I cancel my life insurance in Switzerland?

With a term life insurance, the coverage simply ends and there’s no refund.

With a mixed life insurance, you receive the surrender value, but you’ll lose a significant amount due to high up-front fees and administrative costs. The surrender value equals your paid premiums minus the risk premium and fees.

In many cases, it can make more sense to invest the savings portion elsewhere - even if you lose money upfront. But if your policy is about to end soon, it might be smarter to keep it rather than cancel it.

You can also look into freezing your premiums (premium suspension). That way, you stop paying but keep the policy until maturity, which may be better than canceling if the loss is too high.

Bottom line: Don’t cancel without weighing your options carefully.

Can I have multiple life insurance policies at the same time?

Yes, in Switzerland you can hold multiple policies, for example a term life policy for a mortgage and a disability policy. But be careful not to over-insure yourself and pay for coverage you don’t actually need.

It’s important to review which risks are already covered through AHV, your pension fund (PK), and accident insurance (UVG). This can be evaluated with a professional pension analysis.