40% become unable to work: How to protect yourself with disability insurance in Switzerland

Imagine waking up one day and no longer being able to work – due to burnout, a serious illness, or an accident. This risk is more common than you might think: around 40% of working people in Switzerland will become unable to work at least once during their lifetime.

And here’s the problem: State benefits from the AHV and pension fund often aren't enough to cover your fixed costs or maintain your standard of living.

The solution? Disability insurance – it closes your income gap when fate strikes and you can’t work due to health reasons.

In this article, you’ll learn:

- Why it’s important to think about disability – even if you’re perfectly healthy

- How to identify your personal pension gap

- The role that disability insurance plays

- And what self-employed individuals especially need to watch out for

Table of Contents

- Why you should think about disability even if you’re healthy

- How to find out if you have a disability coverage gap

- Close your gap with disability insurance

- What does disability insurance cost?

- Special case: Self-employed individuals

- Conclusion on disability insurance

- FAQs on disability insurance

Why should I think about disability even if I’m healthy?

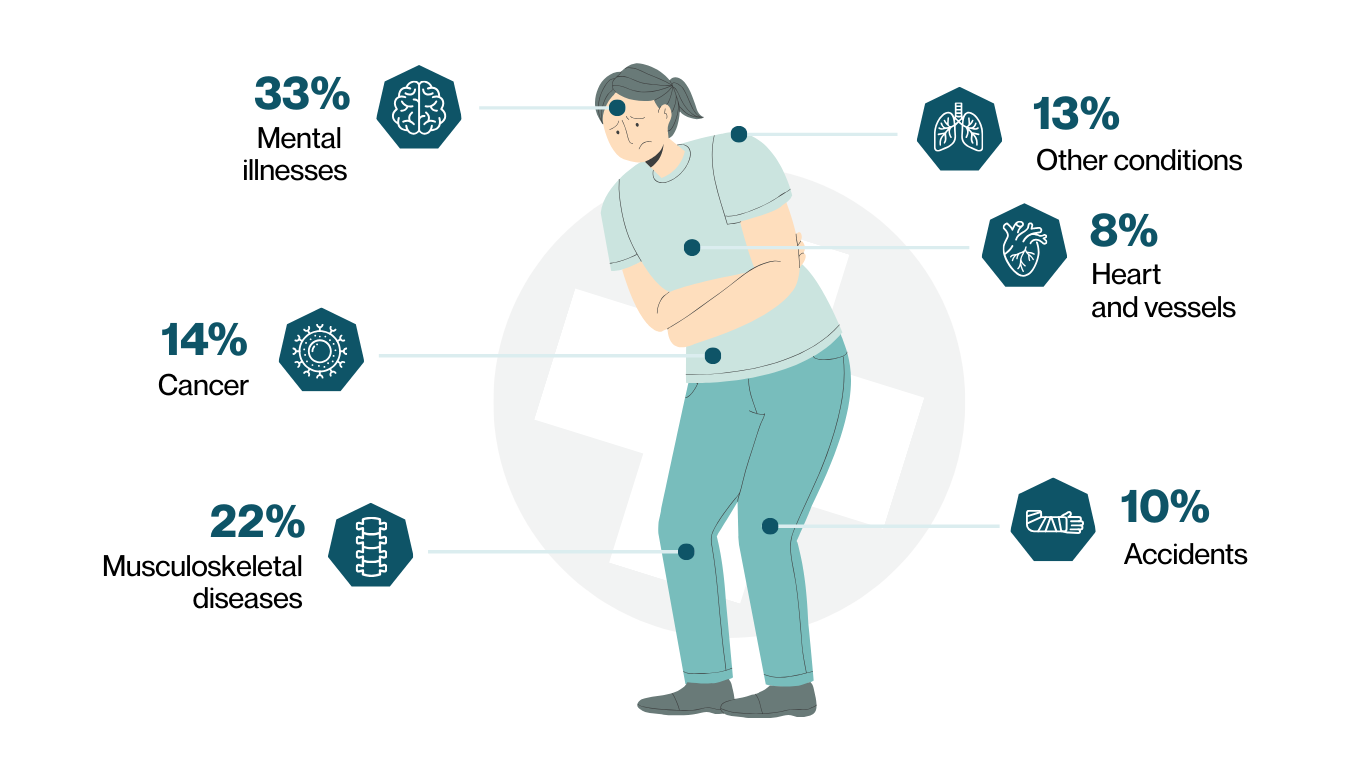

Besides the risk of aging, there is another, more immediate risk: the risk of occupational disability. This risk arises when you can no longer work long-term due to an accident or illness. It is often underestimated, even though around 40% of working people in Switzerland become occupationally disabled at least once in their lifetime. The main causes are typically mental health issues, followed by musculoskeletal disorders and cancer. Accidents account for only 8% of disability cases.

What happens if you become unable to work?

In principle, you receive 100% of your salary from your employer as continued wage payment — depending on your years of service and your canton.

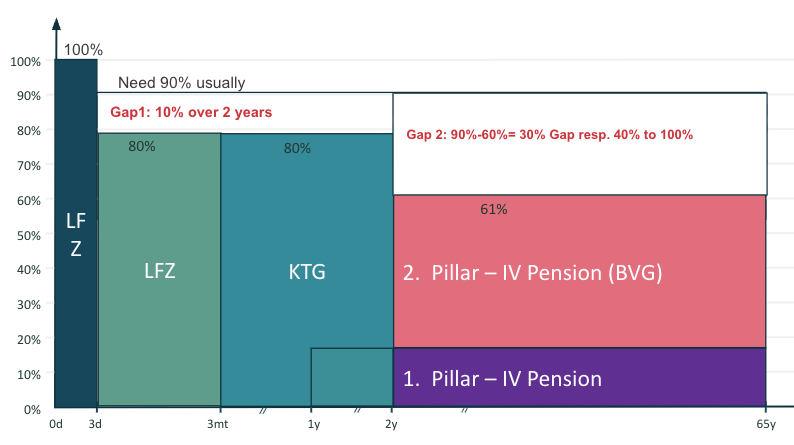

In Case of Illness

In the case of illness, sick pay (KTG) typically amounts to 80% of your salary, paid for up to 720 days (approx. 2 years).

After 1 year of being unable to work, you are entitled to a disability pension (IV) from the AHV, plus a child pension if you have children under 18 or under 25 who are still in education. However, note that the IV pension may only be paid starting in year 2, even if the entitlement begins earlier.

After 2 years, you would receive:

- the AHV IV pension + child pension

- occupational pension (PK) disability pension + PK child pension.

An IV pension is only paid if you are at least 40% disabled. The amount of the pension depends on the degree of disability. You only receive the full IV pension (from AHV and PK) starting at 70% disability.

The amount of your full PK IV pension is listed in your pension fund certificate. The amount of the AHV IV pension is calculated the same way as a normal AHV pension.

Based on this information, you can calculate the coverage gap you would face if you became unable to work due to illness.

In Case of Accident

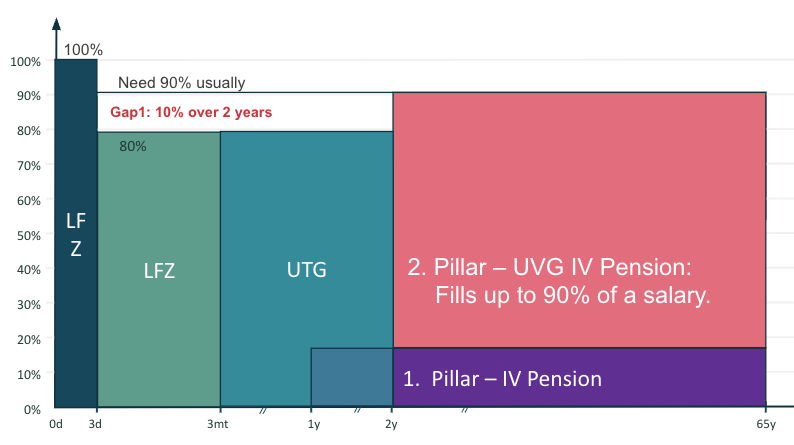

In the event of an accident, after 3 days of continued salary payment, you receive accident daily benefits which typically amount to 80% of your salary, paid for up to 720 days (approx. 2 years).

After 1 year of being unable to work, you are entitled to:

- a disability pension (IV) from the AHV

- plus a child pension, if applicable (same as in the case of illness).

Again, the IV pension might only start being paid from year 2, even if you're already entitled to it.

After 2 years, you would receive:

- the AHV IV pension + child pension

- the accident insurance (UVG) disability pension.

Typically, the IV + child pension and the UVG IV pension combined cover 90% of your salary, up to a salary ceiling of CHF 148,200

(Some employers may insure a higher salary ceiling.)

The IV pension is only paid if you are at least 40% disabled.

The amount depends on your degree of disability, with the full AHV IV pension paid only at 70% disability.

Under the UVG system, however, pensions can be paid starting at just 10% disability.

Based on this information, you can calculate the coverage gap you would face if you became unable to work due to an accident.

How to find out if you have a disability income gap

Order your Individual Account (IK) statement from the AHV or compensation office, your pension fund statement and regulations, and possibly any life insurance documents.

Calculate how much you would need to cover your living expenses if you could no longer work. (Estimate: about 90% of your current income.)

Now determine your income gap by noting how much your 1st pillar (AHV), 2nd pillar (pension fund), and possibly 3rd pillar (e.g. life insurance) would pay you in case of disability.

Do this calculation once for accident and once for illness (e.g., depression, burnout). As mentioned: in case of illness, refer to the IV pension in your pension fund statement; in case of accident, refer to the benefits from accident insurance (UVG).

Add your IV pension + pension fund IV pension in case of illness and subtract your estimated living expenses (approx. 90% of your current income). For accidents, add the IV pension + UVG benefits and then subtract 90% of your income.

Whatever is left is your gap (one for accident, one for illness) – the difference between what you’d receive and what you’d need to live on if you couldn't work.

… and that’s what you need to close!

Close your gap with a disability insurance

If you find a gap in your coverage for accident or illness (almost everyone in Switzerland has one), it’s important to close it using a disability insurance policy.

This insurance pays a monthly pension if you become temporarily or permanently disabled due to illness or accident. It makes sense if your 1st and 2nd pillar disability benefits are too low to cover your living costs.

Already have life insurance? Then check if a disability add-on is already included.

How much does disability insurance cost?

This depends mainly on the amount of income to be insured (i.e., how much you want the insurance to pay out), the term, and factors like a short waiting period.

Example (Zurich Insurance): A woman born in 1993, non-smoker, working in an office job, wants to insure an annual pension of CHF 30'000.-. With a term of 32 years, the cost would be CHF 1'065,50.- per year, or approximately CHF 83.- per month.

Special case: Self-employed

If you are self-employed, you can join a pension fund, in which case the same rules apply to you as to employees.

If you don’t, you can still contribute to pillar 3a, up to 20% of your income, with a yearly cap of CHF 36'288.-.

However, you’ll need to secure yourself against disability risks through private insurance. This means:

- You should include accident coverage in your health insurance, as this is normally covered by the employer for employees.

- You need to take out a daily allowance insurance (Taggeldversicherung) for illness and accident to cover the first 2 years of income loss.

- After that, you’ll need a disability income insurance, which pays a monthly benefit whether the cause is illness or accident.

Otherwise, you’ll only rely on AHV/IV, which usually provides very limited coverage. You can find more info on pension planning for the self-employed here.

My tip: Always request multiple quotes, as the price differences for the same coverage can be significant.

Conclusion on disability insurance

Most people have a short-term gap of around 20% of their salary in case of accident or illness during the first two years. This can be covered with a temporary disability insurance. If you can manage this gap yourself (e.g., via savings or living on 80% of your salary), you might not need the insurance.

However, most people face a long-term gap after two years in the case of illness. This gap can often be as high as 40%, and that’s where disability insurance makes real sense.

FAQs about disability insurance

When does disability insurance start paying?

Most policies have a waiting period of 12 to 24 months before benefits are paid out. Some insurers offer shorter periods (e.g., 3 months). It’s important to choose the right waiting period depending on how long you could manage your expenses with emergency savings or daily allowance benefits.

What’s the difference between disability insurance and an IV pension?

The IV pension (AHV/IV) is a state benefit that is only paid if you are at least 40% disabled. The disability insurance is a private solution that fills your income gap and can be customized to your needs.

Is disability insurance worth it for self-employed people?

Yes, especially for the self-employed. They aren’t automatically covered by a pension fund. Disability insurance ensures that you’ll have a steady income in case of illness or accident, instead of relying solely on minimal IV payments.

How high should your disability pension be?

It depends on your lifestyle, fixed costs, and what’s already covered by AHV, pension fund, or private insurances. As a rule of thumb, you should ensure your essential expenses (like rent, family, living costs) are covered if you can no longer work.

How do I find the right disability insurance in Switzerland?

Always compare multiple offers, as coverage, premiums, and waiting periods can differ greatly. Pay attention to:

- The insured benefit amount

- The waiting period

- Duration of coverage

- Payout conditions

Use comparison tools like Comparis or consult an independent financial advisor for support.