Swiss Homeowners: What you need to know about the end of imputed rental value (Eigenmietwert)

Last updated: 26.01.2026

If you own a home in Switzerland (or plan to buy one soon) there’s a major tax change coming your way. The long-debated Eigenmietwert (imputed rental value) is being abolished following a nationwide vote, marking one of the biggest shifts in Swiss homeownership taxation in decades. In this article, we’ll break down what the Eigenmietwert is, why it’s being scrapped, what the reform means for your taxes, and how to prepare before the changes take effect.

Table of Contents

- What is the Eigenmietwert (Imputed Rental Value) in Switzerland?

- A short history of the Eigenmietwert

- What is the Eigenmietwert Reform (Eigenmietwert Abschaffung)?

- What the end of Eigenmietwert means for homeowners in Switzerland

- Who benefits, who doesn’t: Winners and losers of the reform

- What you should do now to prepare

- Summary: Key takeaways about the “Eigenmietwert Abschaffung”

What is the Eigenmietwert (Imputed Rental Value) in Switzerland?

Let’s start with the basics, because if you’ve ever scratched your head wondering why Switzerland taxes homeowners as if they were tenants in their own home… you're not alone.

Eigenmietwert, or imputed rental value, refers to a fictitious income that gets added to your taxable income if you live in a property you own.

Yep. The tax office assumes that because you could be renting out your home and earning income from it—but aren’t—they’ll go ahead and pretend you did… and then tax you for it.

Wild? Yes.

Here’s how it works:

- The Eigenmietwert is calculated based on the estimated rental value of your home—typically at least 60% of what the market would pay in rent.

- The cantonal tax offices set the value of the Eigenmietwert, at a minimum of 60% and maximum 70% of the market rate rent.

- This value is added to your annual income and taxed accordingly.

- The upside? You’re allowed to deduct certain things—like mortgage interest and maintenance costs—to soften the blow.

It’s a system that tries to balance the tax advantages of owning a home (like paying lower rent and building equity) with the idea of fairness in the tax system.

But as we’ll see next—it’s also been controversial for decades.

A short history of the Eigenmietwert

Here’s a little fun fact that’s more tax-nerdy than fun, but still kinda fascinating: The Eigenmietwert wasn’t always part of Swiss tax law. In fact, it started off over 100 years ago as a “temporary” tax during World War I. The idea? To make up for lost customs revenue while the economy took a hit.

But like so many “temporary” things in life (hello, Ikea shelves that are still standing 8 years later), the tax stuck around.

Let’s dive in.

In the 1930s: The global economy is in chaos. Switzerland introduces the tax. This time as a crisis levy to stabilize federal finances. Originally, it was supposed to expire in 1938… then it got extended. And extended again.

In 1958, the people and the cantons voted to make it official. What started as a stopgap during wartime became a permanent feature of Swiss tax law. And now - almost 70 years later - it was voted out.

Over the last few decades, Eigenmietwert has been one of the most hotly debated policies in Swiss tax law. Here's why:

- It feels counterintuitive: People are taxed on income they never actually receive (fictitious income).

- It discourages homeownership: Especially in a country where fewer than 40% of people own their own home.

- Having an “Eigenmietwert” favours those with large mortgages, who can claim more deductions—while punishing those who’ve paid off their homes. It’s about to change.

Reform proposals have been floated again and again… and again. Some cantons even tried to push ahead with changes on their own. But nothing ever stuck—until now.

What is the Eigenmietwert Reform (Eigenmietwert Abschaffung)?

After years of debate, petitions, and political tug-of-war, the Swiss people have officially voted in favor of a tax reform that will abolish the Eigenmietwert—at least for first homes.

This vote marks one of the biggest shifts in Swiss homeownership taxation in decades.

On 28 September 2025, Swiss voters approved a federal-level reform that includes:

- Scrapping the Eigenmietwert for owner-occupied primary residences (e.g. if you’ve bought your first house and are living in it)

- Introducing a new Objektsteuer (property-based tax) on second homes

- Removing many of the deductions homeowners currently benefit from

This reform only passed because the majority of voters—and cantons—said YES at the national level. Without this approval, the Eigenmietwert would’ve remained intact.

When will the changes happen?

Not overnight. The earliest the reform will come into effect is 2028, which gives homeowners (and the tax authorities) time to prepare and adjust.

What exactly is changing?

Here’s a breakdown of the big shifts:

|

What Stays |

What Goes |

|

Rental income on investment properties stays taxable |

Eigenmietwert on primary residences - so the fictive salary increase: gone (yipee!) |

|

Deductibility of mortgage interest for rental properties |

No more mortgage interest deductions on primary residences (sniff) |

|

Some cantonal deductions may remain |

No federal deductions for maintenance or energy upgrades (sniff) |

|

“Denkmalpflege” (heritage protection) costs still deductible |

|

|

New buyers: Can deduct some mortgage interest for 10 years |

Energy efficiency + demolition costs: no longer deductible |

For homeowners, this means less complexity in filing taxes, but also fewer ways to reduce taxable income.

What the end of Eigenmietwert means for homeowners in Switzerland

So, what does the Eigenmietwert Abschaffung actually mean for you as a homeowner?

Short answer: It depends. Long answer: Let’s break it down.

First homes (owner-occupied)

No more imputed rental income = lower taxable income. That’s the good news, especially if your mortgage is small or paid off.

But here’s the trade-off:

- You can no longer deduct mortgage interest or maintenance costs

- Energy-efficient renovations? Also no longer deductible at the federal level

- Exception: If you recently bought your home, you can still deduct a portion of your mortgage interest for 10 years

Bottom line: If your home is low-maintenance and you’ve already paid off most of your mortgage, you’re likely to benefit. If you're still deep in debt or planning major renovations? Not so much.

Second Homes

The new system introduces a property-based tax (“Objektsteuer”) for second homes, replacing the imputed rental value approach.

This means:

- You’ll still pay taxes on second homes

- But it’s based on the property value, not fictional rent

- Mortgage interest deductions for second homes may still apply, depending on cantonal rules.

Rental Properties

No changes here. If you rent out property, you’ll continue to:

- Pay tax on actual rental income

Deduct mortgage interest, maintenance, and related costs

While the federal deductions are getting slashed, some cantons may still allow deductions for things like:

- Property maintenance

- Mortgage interest

- Renovations

So it’s essential to check what’s happening in your canton, because the exact financial impact may vary depending on where you live.

Who benefits, who doesn’t: winners and losers of the reform

Let’s be real: Every tax reform creates winners and losers. And the Eigenmietwert Abschaffung is no exception.

Depending on your financial setup, location, and homeownership status, you’ll either breathe a sigh of relief—or be digging out the calculator (and a few curse words).

Who benefits from the reform?

You’re more likely to come out ahead if you:

- Own your home outright or have a small mortgage: You’re no longer taxed on imputed rental income and you weren’t deducting much interest anyway.

- Are retired or near retirement: Retirees with fully paid-off homes and limited renovation needs will likely see lower taxable income and fewer headaches.

- Just bought a home: You’ll still be able to deduct some mortgage interest for 10 years, meaning a temporary win.

- Have minimal maintenance costs: Less need for deductions = less to lose.

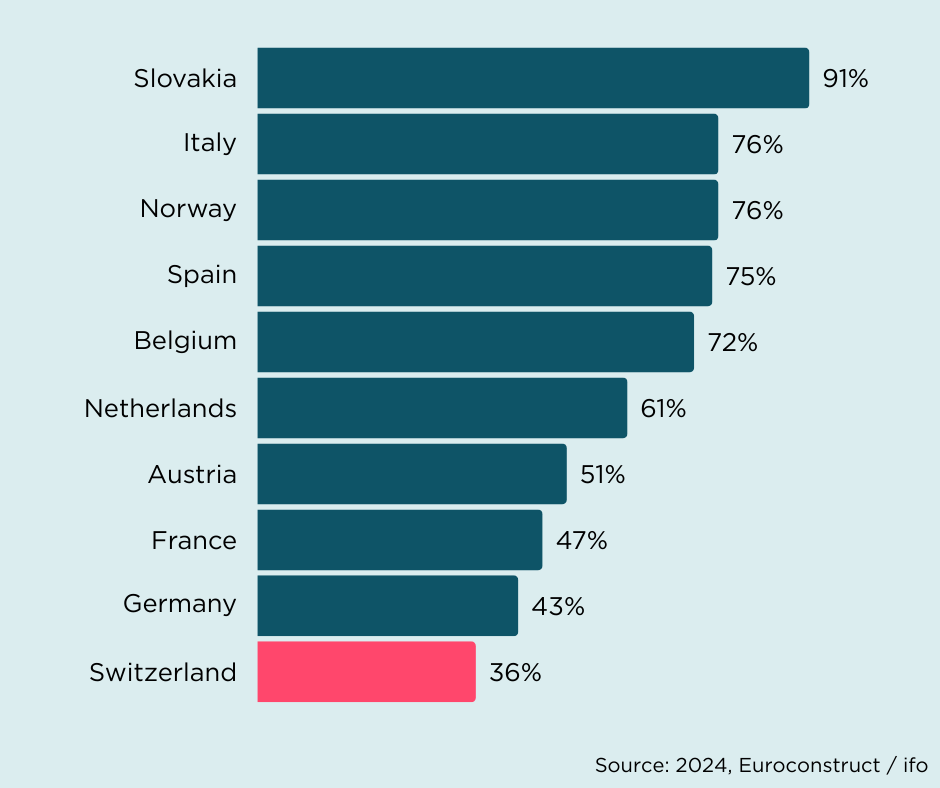

But here’s the inconvenient truth: Young buyers and first-time homeowners are still at a disadvantage.

Let’s look at the numbers: Switzerland’s homeownership rate sits at just 36% - the lowest in Europe.

The “first-time buyer deduction” is a nice gesture, but it won’t make a big difference in moving the home ownership needle.

Switzerland could take a note out of their neighbor’s books: France encourages home buyers by offering 0% interest Prêt à Taux Zéro+ (PTZ+) mortgages for first-time buyers covering up to 50% and max. EUR 180’000.- and Germany allows tax deductions of services and renovations done on the house up to EUR 1’200.-.

Who loses out?

You might be worse off under the new system if you:

- Have a large mortgage: Say goodbye to those juicy mortgage interest deductions. Your tax bill could rise even if your income doesn’t.

- Are renovating or maintaining an older property: Maintenance and upgrade deductions are going away at the federal level (and possibly at the cantonal level too).

- Use energy-efficient investments to optimize your taxes: No more federal deductions for solar panels, insulation, or eco-friendly upgrades.

If you’ve played the deduction game well until now, the reform may hit your bottom line.

But if you’ve already gone “mortgage-light” and like to keep things simple, you’ll likely benefit. Unfortunately though, going “mortgage-light” (self-financing a high amount and taking on less debt) reduces your available cash for other investments leading to less diversification of your assets.

What you should do now to prepare

Just because the Eigenmietwert Abschaffung won’t take effect until 2028 at the earliest, doesn’t mean you should sit back and wait.

Smart homeowners plan ahead.

Especially when a tax shake-up this big is on the horizon.

1. Review your current tax setup

Take a good, hard look at your:

- Mortgage balance and interest payments

Maintenance costs and renovation plans - Current deductions claimed on your tax return

Knowing where you stand today is the first step to understanding how the reform will affect you tomorrow.

Tip: If you’re unsure what you can currently deduct, a short consultation with a tax advisor or financial planner can pay for itself.

2. Don’t rush to pay off your mortgage

It might seem logical to pay off your mortgage now, especially if deductions are going away, but hold up. Depending on your tax position and interest rates, keeping a mortgage for now might still be smarter.

Example: If you’re still deducting large amounts of interest, paying off your mortgage early could mean higher taxes between now and 2028.

Also, the more you pay off now, the less liquidity you keep for other investments.

3. Talk to a financial or tax expert

Every situation is different. An tax advisor or financial planner can help you:

- Rework your long-term strategy

- Decide how and when to reduce your mortgage

- Plan renovations with an eye on cost vs. tax savings

You don’t need to make big moves today, but you do need a plan. Book a call with me here to discuss your situation!

4. Stay informed on cantonal rules

Cantons may still allow certain deductions even after the federal reform kicks in. So, if you live in Zurich, Geneva, or Appenzell (or anywhere in between)—know your local rules.

The difference could save (or cost) you thousands of francs each year.

Summary: Key takeaways about the “Eigenmietwert Abschaffung”

The Eigenmietwert, Switzerland’s tax on imputed rental value for owner-occupied homes, is officially being abolished following a nationwide vote. Starting no earlier than 2028, homeowners will no longer be taxed on fictitious rental income, but they’ll also lose key deductions, like mortgage interest and maintenance costs. This reform will benefit those with low or no mortgage debt, while potentially increasing the tax burden for heavily mortgaged or renovation-heavy properties. If you’re planning major renovations, consider scheduling them within the next 2 years. Plan ahead - because I’m sure the construction companies and trades are going to be busier than they already are!