Best 3a Pillar providers in Switzerland (2026 comparison)

Last updated: 22.05.2026

If you've started on your financial journey in Switzerland, chances are the 3a pillar is already on your radar. It's one of the most powerful financial tools available to residents here - combining tax savings, investment growth and retirement security in one account. But with a growing list of providers, choosing the right one can feel overwhelming. In this guide, I break down what to look for, compare the top providers side by side, and give you my honest, CFP-based recommendation depending on your personal situation.

Table of Contents

- Quick recap: what is the 3a pillar?

- 2026 contribution limits

- What to look for when choosing a provider

- 3a provider overview: fees, interest and backing

- Which is the best 3rd pillar in Switzerland?

- My recommendations by situation

- New in 2026: retroactive contributions

- FAQs

Quick recap: what is the 3a pillar?

The Swiss pension system runs on three pillars. The 1st is state pension (AHV), the 2nd is occupational pension (BVG), and the 3rd is your private pension - the one you build yourself. The 3a pillar is the tax-privileged version of that private provision.

By contributing to a 3a account, you reduce your taxable income and invest that money in stocks or ETFs - with significantly better returns than a traditional savings account. If you are new to this topic, read my full breakdown of everything you need to know about the 3a pillar here.

2026 contribution limits

The maximum 3a contribution remains unchanged for 2026:

- Employees with a pension fund (2nd pillar): CHF 7'258.- per year

- Self-employed without a pension fund: up to 20% of net income, max. CHF 36'288.- per year

Even if you have multiple 3a accounts, the total contributions across all accounts cannot exceed these limits.

What to look for when choosing a 3a provider

Before diving into the comparison, here are the four criteria I always evaluate:

1. Bank vs. insurance

You can open a 3a account with a bank (traditional or fintech) or an insurance company. My clear recommendation: go with a bank-based solution. Insurance products only make sense if you have a genuine need for a risk product such as disability or death coverage - and that should always come from an independent analysis, not as a default choice.

2. Traditional bank vs. fintech

Traditional banks like UBS, PostFinance or Raiffeisen offer 3a accounts, but fintechs have taken the lead when it comes to fees, investment options and user experience. If you are a long-term investor, the fee difference compounds significantly over time.

3. Investment options

Not all providers allow the same investment strategies. If you want 99% stock exposure, sustainable investing (ESG), or crypto allocation, check whether your provider supports it before committing.

4. Fees

This is where the real difference lies. Even a 0.1-0.2% gap in annual management fees makes a meaningful difference over a 20-30 year investment horizon. The fintechs are generally much more transparent here.

Ready for more financial updates like this one? Subscribe to our newsletter!

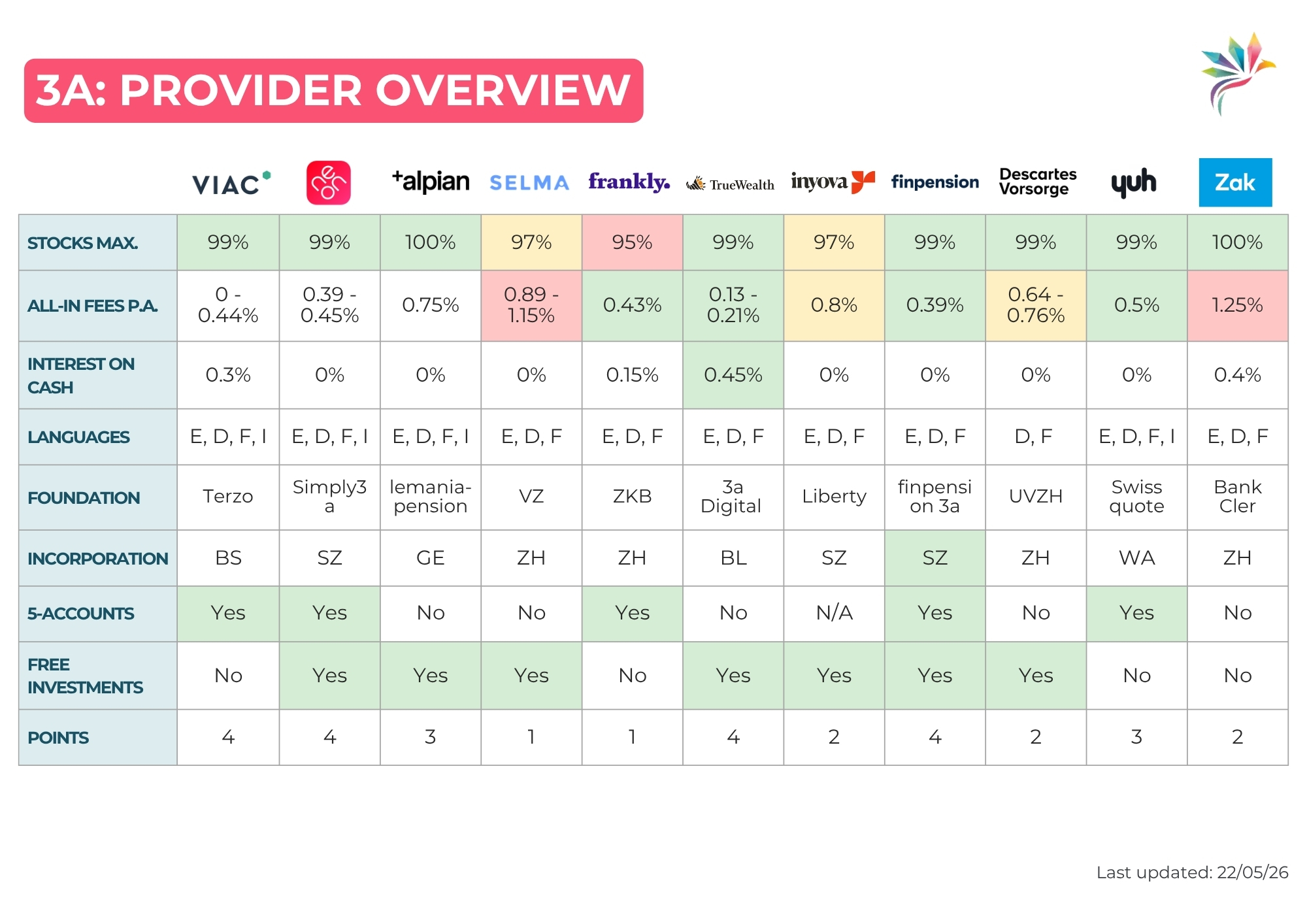

3a provider overview: Fees, interest and backing

Let’s get to it! I’ve compiled an overview of 11 providers that offer very good 3a structures. In the overview you will be able to see how their fees compare, if they give you interest on cash and what bank stands behind the service.

Here are the links for quick access:

- VIAC: viac.ch/en

- NEON: www.neon-free.ch/en/

- alpian: www.alpian.com/3a/alpian-pillar-3a

- SELMA: www.selma.com/de-ch

- Frankly: www.frankly.ch/de/startseite.html

- TrueWealth: www.truewealth.ch

- Inyova: inyova.de

- Finpension: finpension.ch/en (save CHF 25.- in fees with the code "WPMBK8" if you transfer or deposit CHF 1'000.- in the first 12 months!)

- Descartes Vorsorge: descartes.swiss/de-ch

- Yuh: www.yuh.com/de/app/3apillar

- ZAK: www.cler.ch/de/info/zak/zak-vorsorgen

Which is the best 3rd pillar in Switzerland?

Choosing a 3a provider is individual - or as a proper financial planner would say: "it depends." That said, for most investors the answer comes down to two providers: finpension and VIAC. Both are based in canton Schwyz, both allow up to 99% stock allocation, and both have the lowest fees among investment-focused solutions.

The key differences:

- finpension (0.39%): Slightly cheaper, more flexibility for custom strategies, better for aggressive long-term investors. Fees apply to the full portfolio.

- VIAC (0.44%): Invest up to CHF 8'500.- for free; fee applies to any additional franc invested.

- TrueWealth (0.13-0.21%): The lowest overall running costs on the market, however, does not allow for multiple 3a-accounts at once (the platform will open up an additional account for you every year that you are a client).

My recommendations by situation

You are an expat and don't know how long you'll stay in Switzerland

Go with a provider based in canton Schwyz - finpension or VIAC both qualify. When you eventually leave Switzerland and withdraw your 3a, source taxes apply. Canton Schwyz has the most favourable source tax rates in the country, which can mean a meaningful saving on withdrawal.

You want maximum investment flexibility

finpension. You can invest up to 99% in stocks, the fees are the lowest among investment-focused providers at 0.39%, and the platform supports fully custom strategies.

You are new to investing and want simplicity

VIAC or finpension. Both good default choices for conservative to moderate investors who don't want to build a custom strategy from scratch.

Two situations where you should hold off on 3a:

- You are taxed at source and earn under CHF 120'000.-: Without a tax declaration, you cannot claim the deduction - so the main benefit disappears. Get that sorted first.

- You don't have your emergency fund in place: The 3a is locked until 5 years before retirement age (with exceptions). Do not tie up money you might need short-term.

New in 2026: retroactive contributions

This is genuinely new and worth knowing about. Starting in 2026, you can for the first time make retroactive catch-up contributions to your 3a account for previous years where you did not contribute the maximum amount.

Two important rules:

- You must first contribute the full maximum for the current year (CHF 7'258.- in 2026) before any retroactive payments are allowed.

- Gaps can only be closed from the 2025 contribution year onward - earlier gaps cannot be retroactively filled.

This is a meaningful change for anyone who missed contributions during career breaks, parental leave or periods of self-employment.

FAQs

How much can I contribute to the 3a pillar in 2026?

CHF 7'258.- for employees with a pension fund. Self-employed individuals without a 2nd pillar can contribute up to 20% of their net income, capped at CHF 36'288.-. These limits apply across all your 3a accounts combined.

What is the best pillar 3a provider in Switzerland?

For most investors, the answer is finpension or VIAC - both based in canton Schwyz, both offering 99% stock allocation at low fees. For long-term savers prioritising fee efficiency, TrueWealth (0.13-0.21% overall costs) is the strongest option. The right choice depends on your situation - see my recommendations above.

Is VIAC or finpension better?

For aggressive long-term investors, finpension has a slight edge - lower fees (0.39% vs. 0.44%) and more flexibility for custom strategies. For conservative investors who keep part of their portfolio in cash or bonds, VIAC's fee structure (only charged on the invested portion) can work out cheaper.

Can I have multiple 3a accounts?

Yes - and it's worth doing. Having multiple accounts lets you stagger withdrawals at retirement, which reduces your tax burden (Switzerland taxes 3a withdrawals separately at a reduced rate). A common rule of thumb: once a single account reaches CHF 50'000.-, open a second one.

What happens to my 3a if I leave Switzerland?

You can withdraw your 3a savings when permanently leaving the country. The payout is taxed at source, and the canton where your provider is registered determines the tax rate. Canton Schwyz has the most favourable rates - which is why expats should default to VIAC or finpension.

Can the self-employed open a 3a account?

Yes. If you are self-employed without a 2nd pillar pension fund, you benefit from the higher cap of CHF 36'288.- (max 20% of your profit) per year - five times the standard employee limit. This makes the 3a an especially powerful tax optimisation tool for freelancers and business owners.

Should I choose a bank or insurance for my 3a?

In most cases: a bank or fintech. Insurance-based 3a products are often inflexible and more expensive. The only exception is if you have a genuine, independently confirmed need for a risk product like disability or death coverage - and even then, that analysis should come first.