Building a solid foundation for retirement: The power of Switzerland's 3a Pillar (Säule 3a)

The 3rd pillar (Säule 3a) in Switzerland is a voluntary pension scheme that operates alongside the mandatory state pension (1st pillar) and the occupational pension (2nd pillar). By making regular contributions to your 3rd pillar accounts, you can purposefully set aside funds for your retirement and take advantage of attractive tax benefits – sounds good, right? The 3rd pillar provides a diverse range of investment options, including savings accounts, securities, investment funds, and life insurance products, giving you the flexibility to tailor your investment strategy based on your risk tolerance and long-term objectives. The 3rd pillar plays a crucial role in securing your financial well-being during retirement, empowering you to actively shape your financial future. The 3rd pillar splits into two different subsections, called the 3a (tied pension provision) and 3b (free pension provision), but in this article I will focus primarily on the 3a subsection. Keep reading so that you don’t miss out on this great investing tool in Switzerland!

Table of contents

- Understanding the 3rd Pillar (Säule 3a) in Switzerland: Securing Your Retirement Finances

- Advantages of the 3a pillar (Säule 3a)

- Strategies for your 3a investment

- Can I have more than one 3a account?

- Main provider for the 3a retirement fund

- When shouldn't you pay into the 3a?

- Final words about 3a in Switzerland

Understanding the 3rd Pillar (Säule 3a) in Switzerland: Securing Your Retirement Finances

Through the 3a pillar, you can make regular contributions to a dedicated retirement account. These contributions are tax-deductible, meaning you can lower your taxable income and enjoy immediate tax savings – we love that! This incentivizes you to save more for your retirement while optimizing your overall tax situation.

Key facts about the 3a pillar:

- It is tied to the Federal Law on Occupational Retirement, and Disability Pension Plans (BVG).

- It primarily applies to employees who are already insured under the mandatory occupational pension scheme (2nd pillar).

- Contributions to the 3a pillar are tax-deductible, subject to annual contribution limits. In 2025, employees are allowed to contribute a maximum of CHF 7’258.-. Self-employed without a state pension scheme are allowed to invest up to 20% of their yearly earnings capped at a maximum of CHF 36’288.- per year.

- The funds in the 3a pillar can be used for the acquisition of residential property, starting your own business or moving out of Switzerland.

- The funds can be paid out in the form of a pension (if it’s a life insurance product) or a one-time lump sum, subject to certain conditions.

Advantages of the 3a pillar (Säule 3a)

One of the key advantages of the 3a pillar is the range of investment options it offers. You have the flexibility to choose from various financial instruments, including savings accounts, bonds, stocks, investment funds, and insurance products. This allows you to customize your investment strategy based on your risk tolerance and long-term goals. Whether you prefer a conservative approach or are willing to take on more risk for potential higher returns, the 3a pillar enables you to align your investments with your individual preferences.

Furthermore, you benefit from a tax benefit as you pay in. The contributions made to the 3a account reduce your taxable income, which leads to more money in your pocket. You could save approximately CHF 1’750.- CHF in taxes per year when contributing the full amount of CHF 7’258.-.

Strategies for your 3a investment

There are several strategies that can be employed when utilizing the 3a pillar (Säule 3a) in Switzerland to optimize retirement planning. Here are some common strategies:

- Start early: It is advisable to start saving for retirement through the 3a pillar as early as possible. The earlier you begin, the more time your contributions have to grow through compounding and build a larger nest egg.

- Regular contributions: Making regular contributions to your 3a pillar account allows for consistent wealth accumulation. Setting up automatic payments is recommended to ensure you consistently contribute funds to your 3a pillar accounts.

- Contribute as much as possible to the 3rd pillar. By doing so, you improve your retirement savings and save taxes. The tax savings amount to approximately CHF 200.- to CHF 400.- per CHF 1’000.- contributed, depending on taxable income and place of residence. For employed individuals who are insured under an occupational pension scheme, the maximum contribution limit for 2025 is CHF 7’258.-. For employed individuals without an occupational pension scheme, the maximum contribution is 20% of net income, but no more than CHF 36’288.-.

- Diversify investments: Diversifying your investments within the 3a pillar can help spread risk and maximize potential returns. Consider allocating funds across different asset classes such as stocks, bonds, investment funds, and even real estate to maintain a balanced and resilient portfolio against market fluctuations.

- Seek expert advice: Consulting with a financial advisor retirement planning expert can be beneficial. They can assist in selecting the best investment strategy, assessing risk profiles, and planning your 3a pillar effectively. If you have a choice, always opt for an independent advisor (like me) thus not employed by a bank or insurance.

- Utilize tax advantages: Contributions to the 3a pillar are tax-deductible. It is important to understand the current tax regulations and benefits to maximize the tax advantages of your 3a pillar.

- Consider investment horizon and risk tolerance: Depending on your individual investment horizon and risk tolerance, you can adjust your investment strategy. If you have many years until retirement, you may consider slightly more aggressive investments to potentially achieve higher long-term returns. As you approach retirement, however, a more conservative investment strategy may be prudent to protect your capital.

- A 3rd pillar invested in securities yields better returns in the long run than a savings account. Especially now, considering that the inflation in Switzerland has risen over the interest rate, you should consider the option of investment solutions: With a 3a investment solution, you take on more risk compared to a 3a savings account, but the long-term returns are generally significantly higher. Let's consider a comparison: If you had been contributing the maximum amount for employed individuals with a pension fund into a 3a savings account every year for the past 30 years at 2,1% interest, they would have a balance of nearly CHF 238’000.- today. With a securities solution that invests 40 percent in stocks, the balance would be at least CHF 57’000.- higher assuming 5% yield (the money you earn on your investment) and 0,8% fees per year. You can follow the whole calculation here.

Can I have more than one 3a account?

Yes! There is basically no limit to how many 3a accounts you can open (depends on the canton you’re in – this is correct for Kanton Zürich). However, many providers will limit you on how many accounts you can open with them. Depending on where you live, having multiple 3a accounts can be a real tax-saving mechanism because of a phenomenon called progressive taxation. Progressive taxation refers to the fact that your tax rate increases as your taxable amount increases. The more you make, the more taxes you pay.

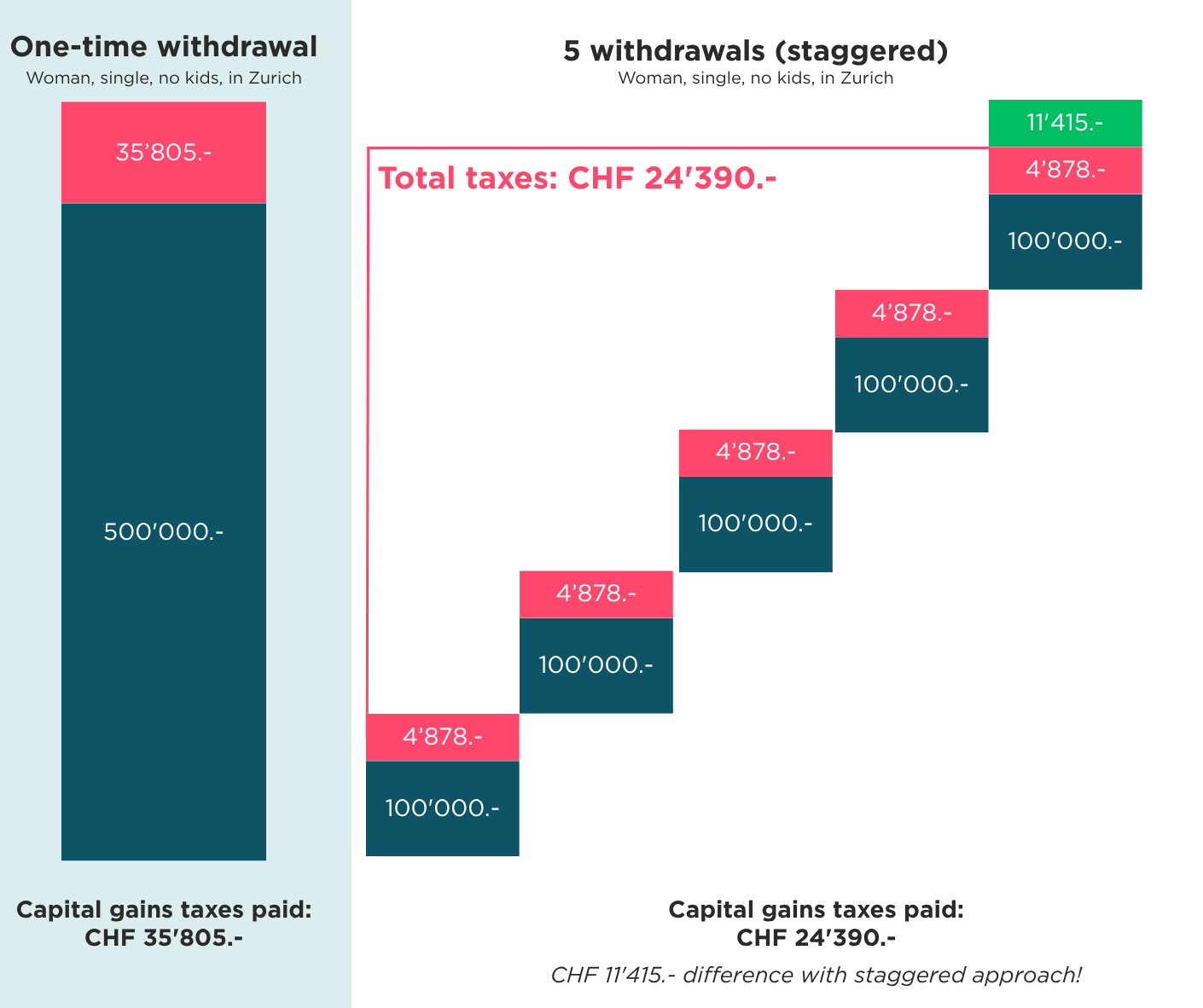

Let’s say you’ve saved CHF 250’000.- in your 3a account by retirement.

If you withdraw it all at once, boom - your tax rate jumps up because you’re taxed more on more money at once. In our example that means a tax bill of CHF 35’805.- if you had all your money in one account.

⚠️ Remember: 3a accounts need to be withdrawn in full, hence in one go.

If you had all the money in 5 accounts, you would have been able to pull it out over 5 different tax years, thus would have paid 5x CHF 4'878.-, thus total of CHF 24'390.-.

In our example, that leads to a difference of CHF 11’415.-. That is money that you are free to spend and doesn’t go to the state.

All you have to do? Open several accounts. That’s it.

Especially in cantons like Lausanne, Genève, or Schaffhausen it can be very beneficial to create multiple 3a accounts to keep taxes at bay. In other areas you will start to be affected more once your 3a accounts reach CHF 50’000.-.

Also: It gives you the flexibility to withdraw for different purposes. Starting a business, you may withdraw the money from one 3a account to fund your “Einzelfirma” (aka sole property company not GmbH), while staying relaxed, because your other 4 accounts will still be there to pay for your comfy retirement.

Two rules of thumb for you to remember: Firstly, have a minimum 5 accounts and secondly, fill them evenly - don’t wait until one is at a certain size before starting to fill the next - the compounding effects will knock it out of the park if you do that. Find out how your canton is affecting your taxes in this article.

Main provider for the 3a retirement fund

Generally speaking, you have the option between a bank and an insurance provider. There is no definitive answer to the question which option is better for you, because this really depends on what your goals are and what you value more. However, I’m personally a fan of banks in this case. In my opinion, opening up a 3a account with an insurance only makes sense if you are looking to acquire a life insurance, not when you are looking to invest your money and yield significant returns.

The main providers of the 3a pillar in Switzerland, include various financial institutions such as banks, insurance companies, and asset management firms.

If you choose a bank as your provider, you will be flexible regarding your contributions in terms of the amount and the frequency. Also, the flexibility in the withdrawal timing is worth considering. But you need to remember: A bank does not provide you with insurance coverage in case of disability, job loss or death.

With an insurance company you will have the advantage of a premium waiver in case of disability but the dissolution and transfer to other 3a pillar solutions often involve costs. Also, in case of an early termination the buyback value will be reduced. So, a bank would be more flexible and with an insurance or fintech company you will have the bonus of being insured.

The biggest providers if you are looking for a bank would be: UBS, PostFinance, Zürcher Kantonalbank (ZKB) and Raiffeisen. Additionally, there are more and more fintechs entering the market and offering the possibility to use the 3a scheme. They are more flexible and often less pricey than the established banks. Find out more in our extensive 3a provider overview here.

If you think an insurance group would be a better fit for you, the most popular ones are SwissLife, Zurich Insurance Group, Helvetia Insurance, Allianz Suisse and Generali Switzerland.

When shouldn't you pay into the 3a?

There are certain cases when paying into the 3a doesn't make sense, for example if you are taxed at source and earning less than 120'000.- per year. As we've seen, the main 3a benefit is a tax deduction, which you can't benefit from when taxed at source - only when filing a tax declaration. Now, before you jump the gun: Calculate the difference between your current source tax and the traditional tax declaration very carefully! You might be better off not contributing to the 3a and simply investing outside of the 3a pillar instead.

Final words about 3a in Switzerland

If there is one take-away for you it is that the 3a pillar (Säule 3a) plays a crucial role in retirement planning in Switzerland. By taking advantage of its tax benefits and diverse investment options, you can actively save for your retirement and build a secure financial foundation for the future. The 3a pillar offers you the opportunity to customize your retirement savings strategy and ensure a comfortable and prosperous retirement. As you contribute to the 3rd pillar, your savings have the potential to grow over time. Also, your yearly contributions lower your taxable income, which leads to more disposable income for spending or investing. However, unfortunately, you will have to pay capital benefit taxes on the returns generated within the account once you withdraw the money.